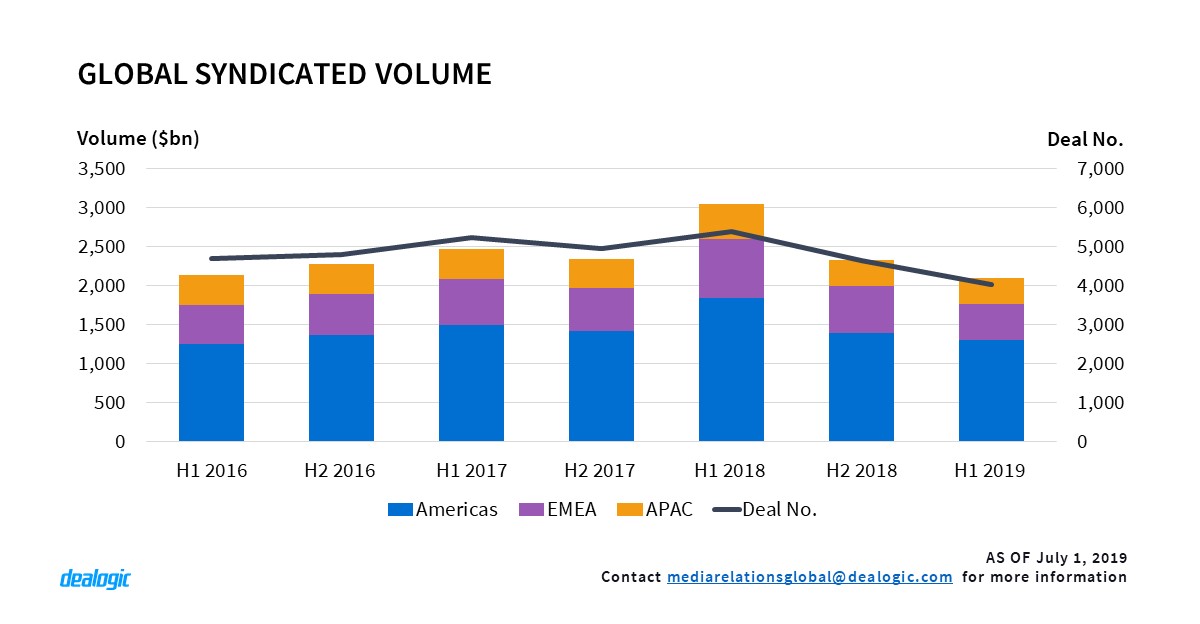

Global loans on a go slow

An unstable economic and political climate driven by US-China trade war jitters, Brexit and Iran, have impacted the loans market. Global syndicated loans volume which totalled $2.09tr via 4,036 deals is at its lowest since H1 2012 and down by 31% on H1 2018. Year on year the EMEA region suffered the sharpest decline in volume, down 40% followed by Americas which witnessed a 29% fall and APAC which dropped by 24%.

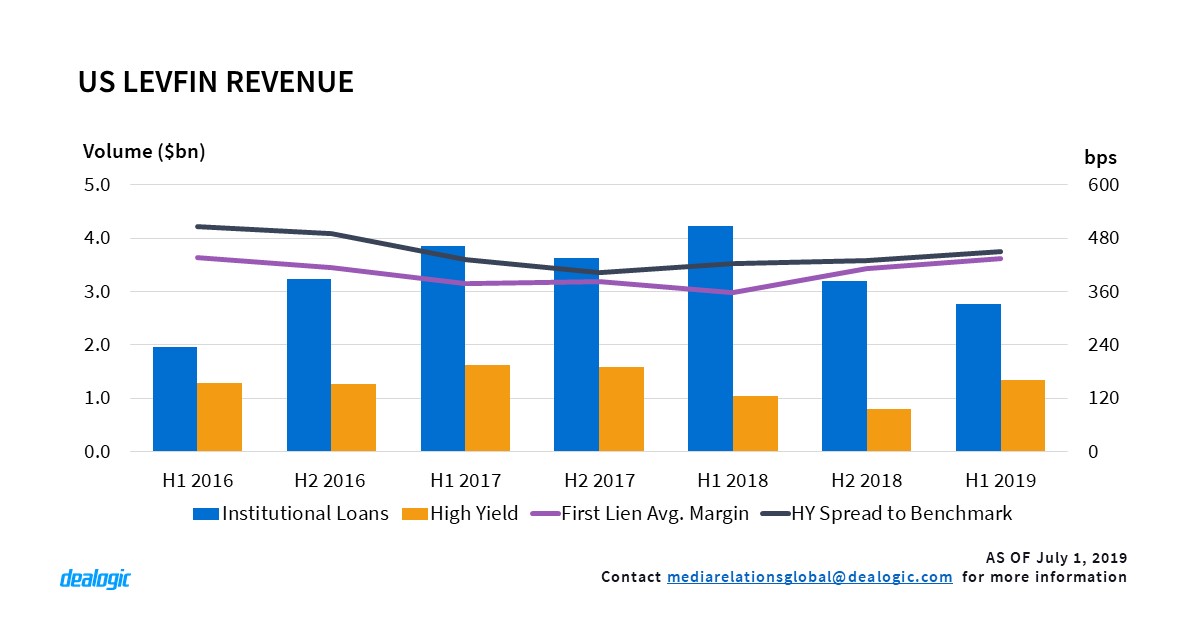

Weak US LevFin Market

Net revenue from US LevFin (High Yield (HY) and loans) shrank to $4.1bn in H1 2019, down by 23% on H1 2018. The decline in revenue generated by banks is driven by a subdued leveraged loans market which saw activity falling from 910 deals in H1 2018 to 411 deals in H1 2019. The rising margins for first lien US levfin loans which jumped from 357bps in H1 2018 to 434bps, did not foster an environment conducive for refinancing and repricing. The market shift in favour of lenders is seen in a growing number of MFN* clauses. Disclosed MFN data demonstrates that the proportion of MFN clauses increased by 10 percentage points from H1 2018.

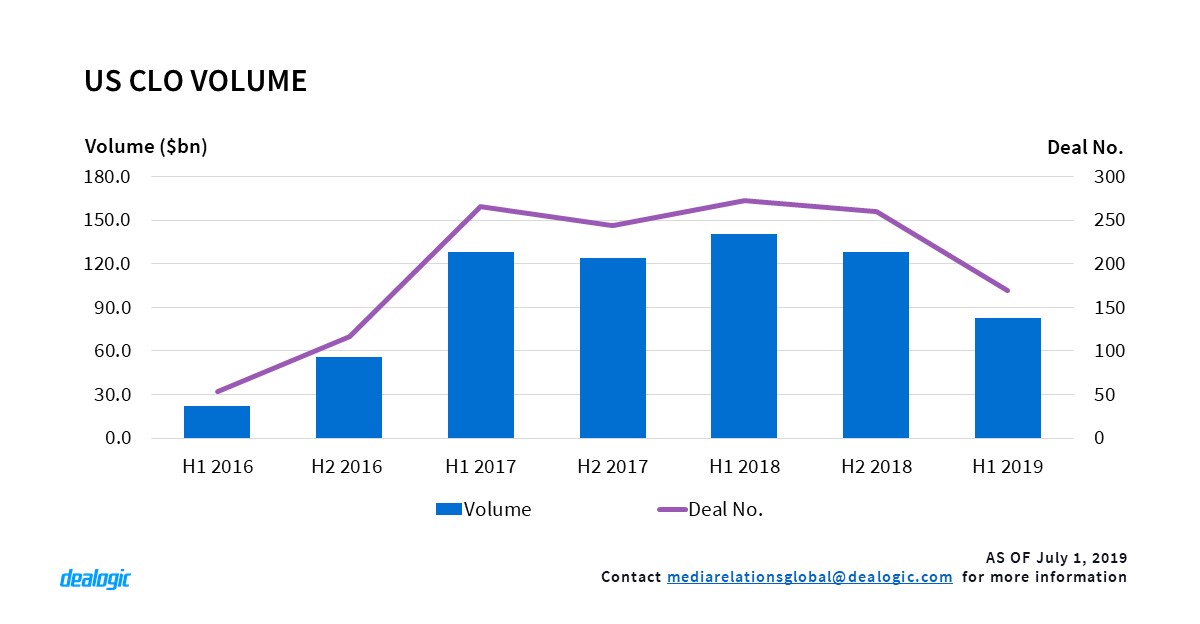

The subdued US LevFin market also coincides with a weaker number of CLOs hitting the market which is at its lowest in terms of volume and activity since H1 2016 ($22.4bn via 54 deals). Year on year CLO issuances declined from $140.6bn via 272 deals (H1 2018) to $82.8bn via 169 deals in H1 2019. The high point remains US HY, which performed solidly in the first 6 months with volume and revenue jumping by 24% and 19% respectively from H1 2018. The US HY product benefited from lower spreads and the resurgence of financial sponsor driven US HY which increased by 90% on H1 2018.

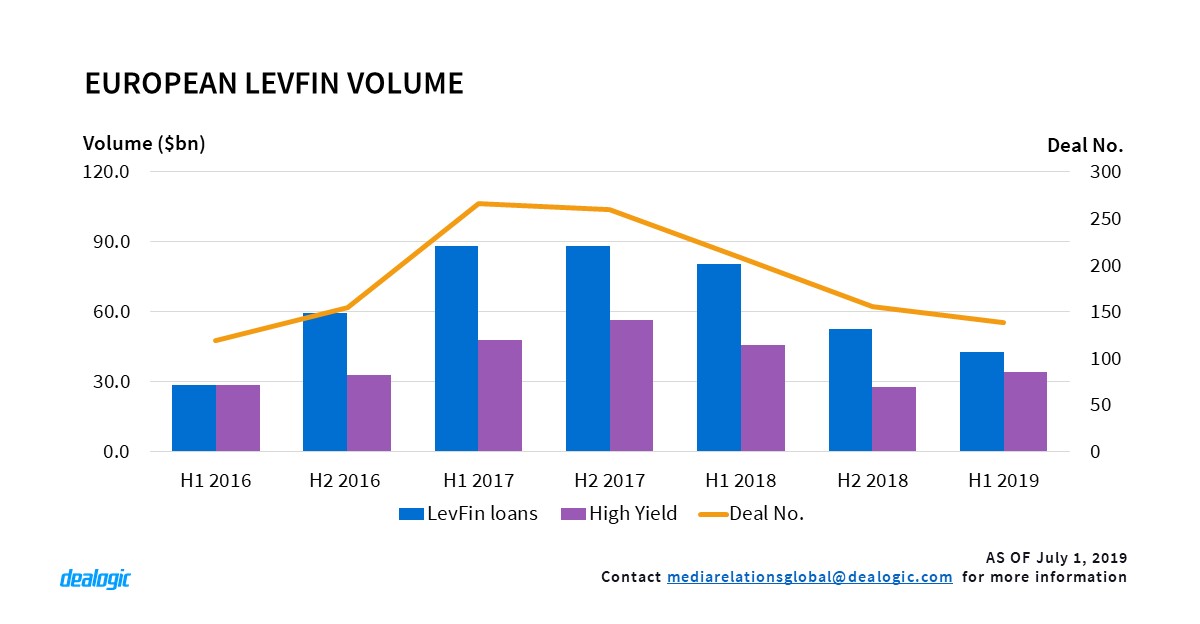

Performance of European HY is even more striking. So far this year, lending volumes and activity are almost on a par with European HY transactions for the same period last year. Compared to H1 2018, activity for European LevFin loans collapsed by 47% to reach only 70 deals. Out of the $42.8bn of volume generated, only 57% came from new deals, highlighting the changing nature of the market. From a revenue perspective, even though HY increased its attributed share of European LevFin wallet to 37.4% in H1 2019 (29.1%, H1 2018), loan issuance remains the major contributor in terms of fees generated in the European LevFin market.

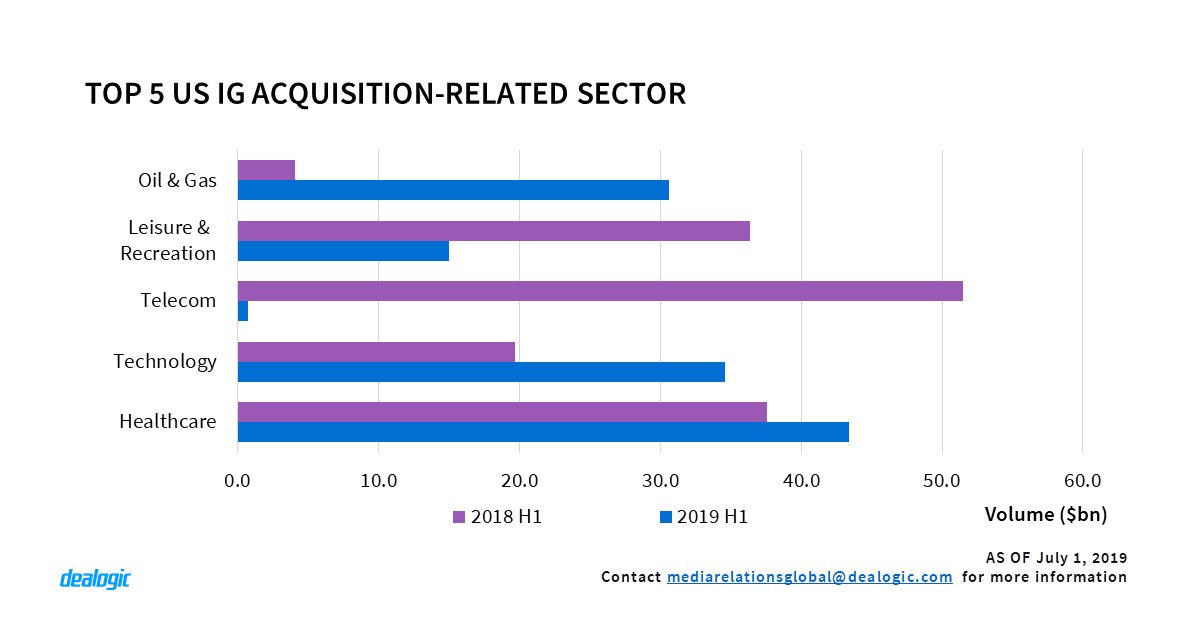

US Marketed Investment Grade (IG) tumbles as acquisition financing stalls

US Marketed IG volume took a dive in the first 6 months of the year, down by 11% on H1 2018. attributed by a fall of 25% in new acquisitions financings. From a sector perspective, Telecom acquisition related financing saw the sharpest fall dropping from $51.5bn to $725m. It is however worth noting that IG Telecoms acquisition financing in H1 2018 was boosted considerably by deals such as Comcast and T-Mobile USA.

While acquisition related lending has been falling, it is important to note that the share of jumbo* IG deals has remained steady. In H1 2019, they accounted for 84.3% of activity, on par with H1 2018.

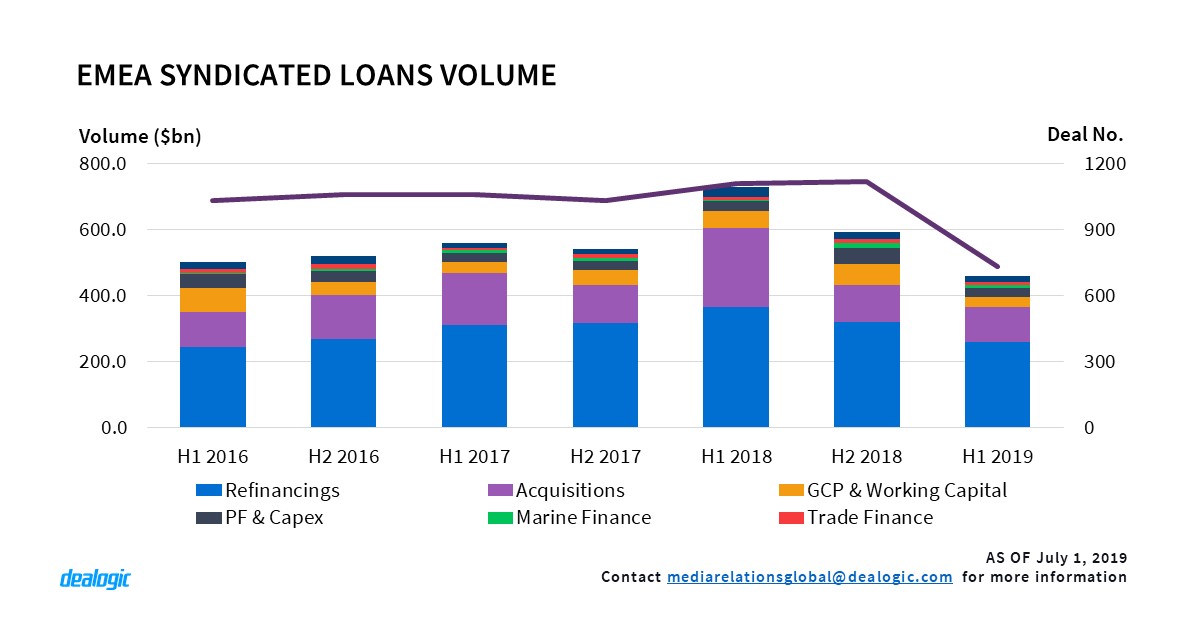

When politics dictates EMEA loans volume

Deals have been scarce in EMEA with only 734 facilities reaching signing date, down by 34% on H1 2018 and the lowest since H1 2009. The current political and economic climate adversely hit M&A-related financing volume and activity which plummeted from $244.7bn to $113.0bn. The reluctance of borrowers to come to the market was further reflected with the huge drop in refinancings and amendments which fell by 29% from H1 2018.

H1 2019 in Europe has also been marked by the growing popularity of ESG linked loans. As climate change and sustainability dominate the political and corporate agendas, there is a growing demand for green and/or sustainable finance. Europe in particular has seen a growth in ESG linked loans which soared from $17.3bn via 14 deals in H1 2018 to $28.9bn via 25 deals in H1 2019.

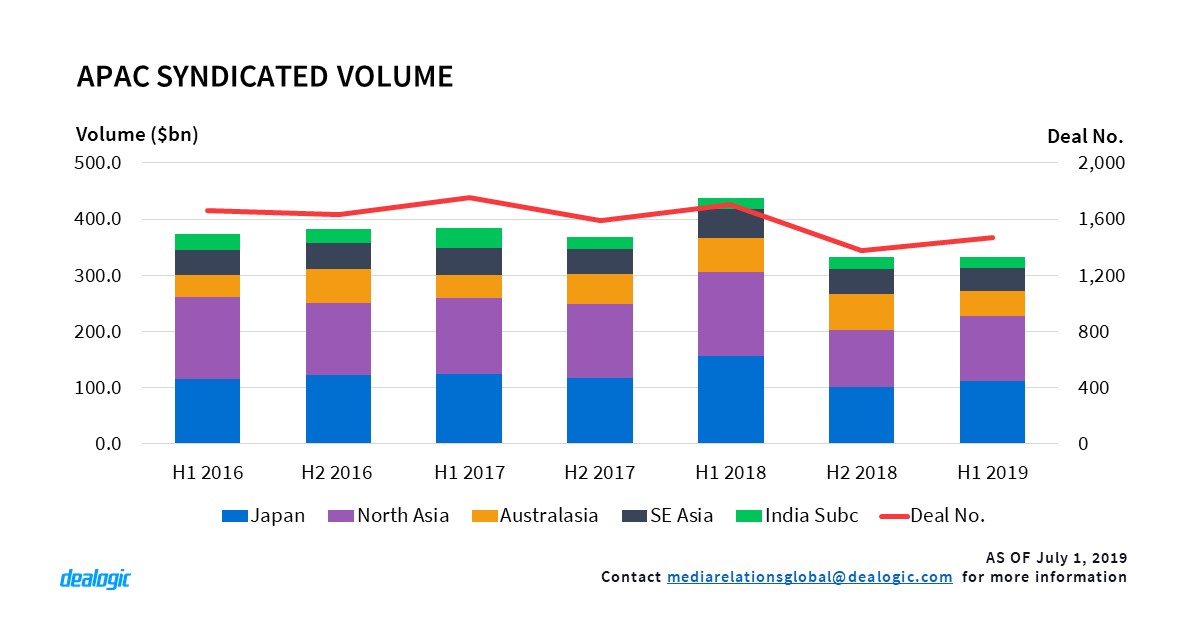

APAC mirrors the global lackluster trends

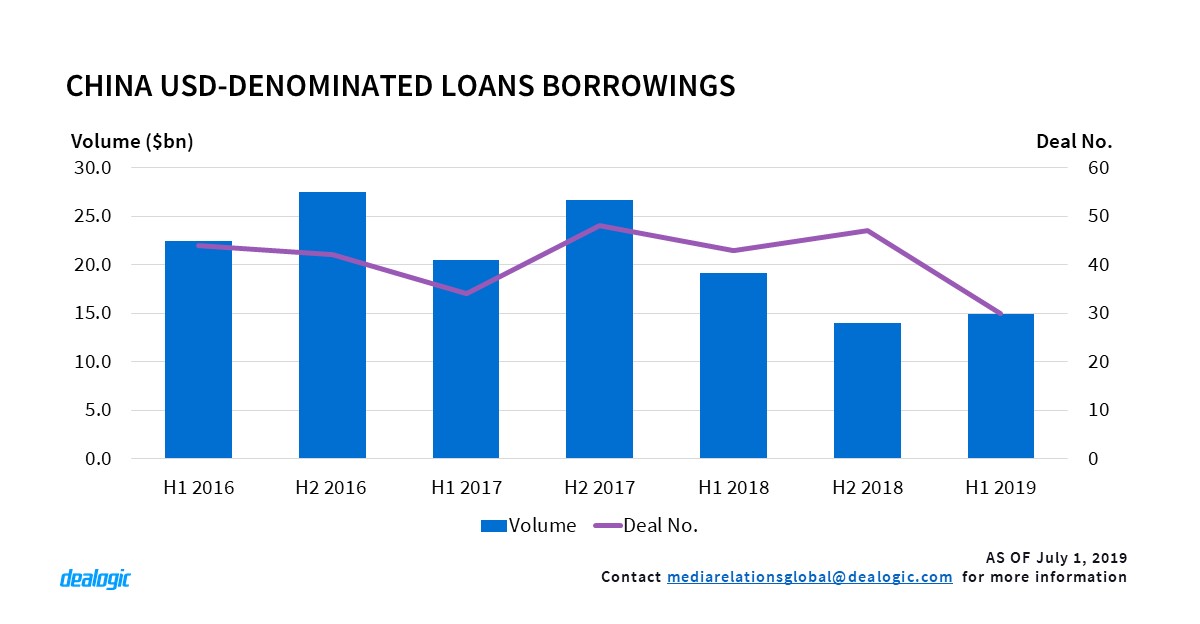

North Asia, Australasia and SE Asia all fell by 22%, 25% and 22% respectively from H1 2018. The Indian sub-continent is the only region to be on par with H1 2018 despite a drop in activity from 83 to 70 deals. The drop in North Asia is driven by a lackluster China onshore market which collapsed from $328.0bn to $192.4bn driven by the general deceleration in project finance and capital expenditure financings for the region. China offshore also tracked downwards with volume declining from $33.8bn to $14.6bn. Since the US-China trade war, there has been a slow down for USD denominated transactions by Chinese borrowers. China USD-denominated lending fell from $19.2bn (H1 2018) to $14.8bn in H1 2019.

Japan also mirrored the current trend of failing volume and activity. As fewer deals hit the market, it was also noticed that jumbo deals decelerated, down by 45% on H1 2018.

– Written by Dealogic Loans Research

Data source: Dealogic, as of July 1, 2019