Global Outlook: FY 2019 Market Drivers

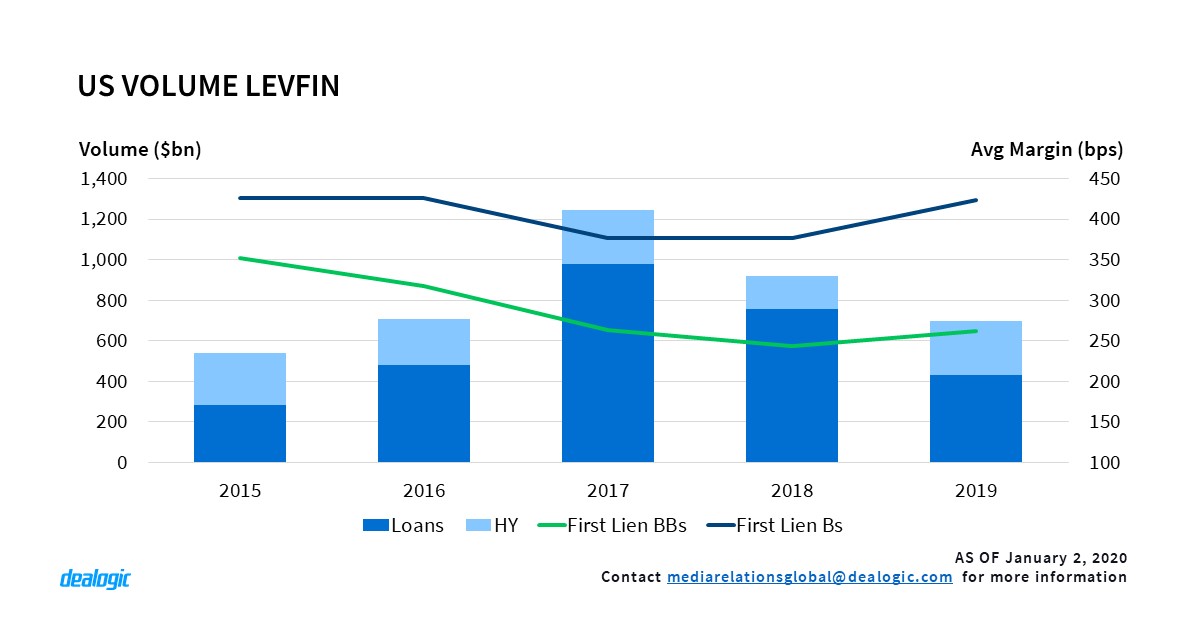

The syndicated loans market had to navigate troubled waters in 2019. Increasing trade barriers, political uncertainty as well as the cyclical and structural deceleration of some major economies impacted both volume and revenue which were down by 15% and 24% respectively year-on-year. Non-Investment grade loans receded at a fast pace with a contraction of 20% from 2018 levels, whilst investment grade was down by 11%. The sharp drop in non-investment grade lending was fuelled by a lack of deals in the US leveraged market which saw activity shrink by 20% from 2018. After feast years in 2017 and 2018, LevFin was less borrower friendly amidst rising concerns about debt levels.

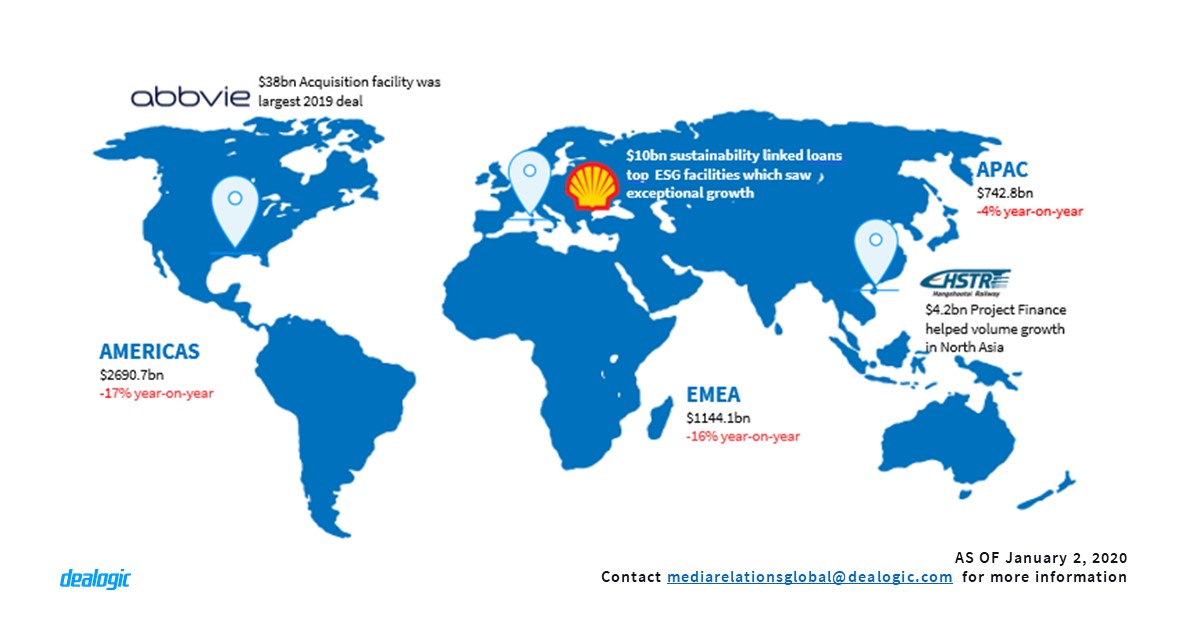

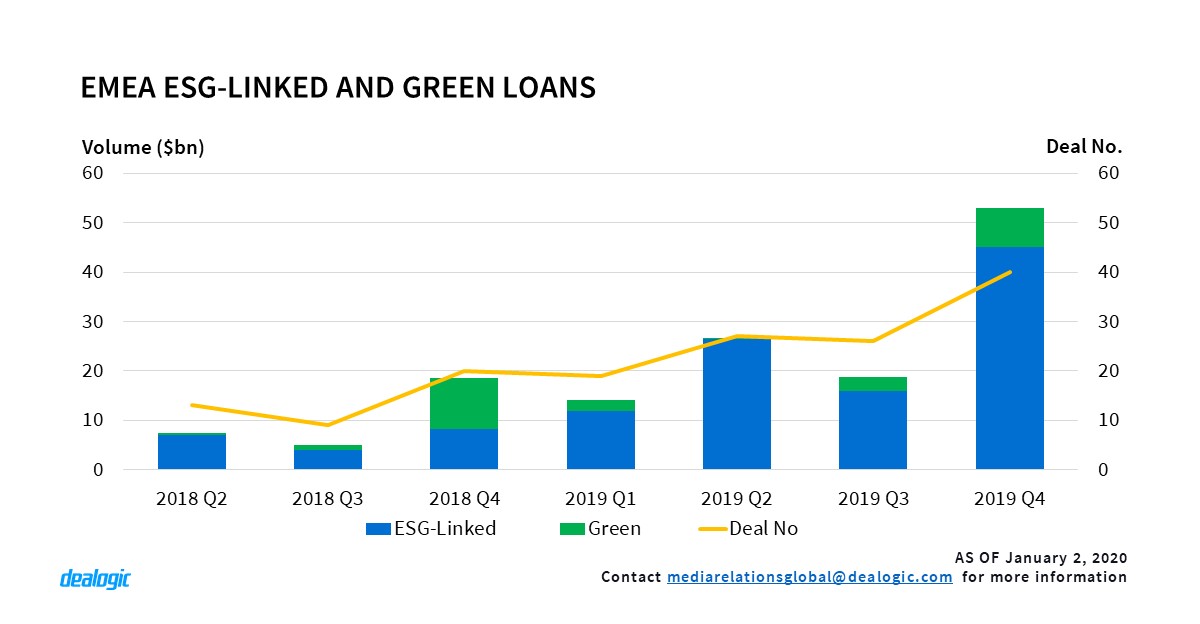

On another front, concerns over climate change and sustainability led to an important market evolution this year. Following in the footsteps of the Bond market, Green and ESG-linked loans gained momentum, especially in EMEA, where volume year-on-year jumped from $41.3bn in 2018 to $112.3bn in 2019. Despite claims of greenwashing, sustainable features in credit agreements are bound to become more prominent.

US LevFIn: A Bifurcated Market

US leveraged finance revenue (Loans & HY) which has been falling for the last 3 years, reached $8.9bn via 1252 deals in 2019 – a decrease of 24% in volume and 29% in activity, year-on-year. Whilst the lower performance in 2018 was attributed to weak demand for HY bonds, 2019 saw a huge decline in loans volume which fell from $756.3bn to $431.6bn year-on-year. Less activity from Financial Sponsors which fell from 1,090 deals (2018) to 631 deals (2019) undeniably drove loan volumes down. Yet despite this, loans continued to be the main driver of LevFin revenue with a 64.1% share. High Yield meanwhile experienced significant growth in 2019, with a 53.7% year-on-year rise in its wallet.

In 2019, the institutional loans market was more lender friendly and as a result, there was a clear bifurcation in loans across different risk levels. One of the more interesting phenomena was the difference in year-on-year change in margins of single-B rated loans versus double-B rated loans. Whilst both on average experienced increases in margin, the scale of those increases was very different.

On average, first lien loans with a single-B rating saw margin increase from 376bps in 2018 to 423bps in 2019, a 13% flex year-on-year. On the other hand, double-B rated first lien loans only saw a slight increase in margin from 244bps in 2018 to 262bps in 2019. This tells us that lenders required a greater increase in margin for the comparatively riskier single-B loans, compared to the double-B rated loans. This can be attributed to investors becoming nervous about how long US economic expansion can last, as geopolitical uncertainty increases with the trade war unresolved and the 2020 Presidential election approaching.

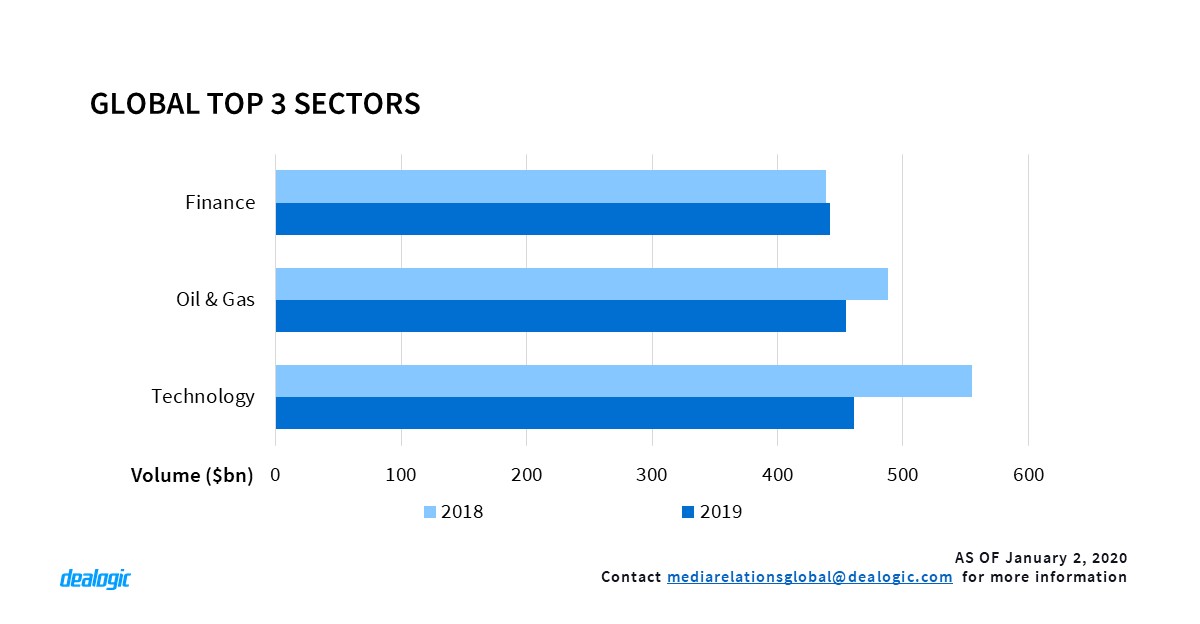

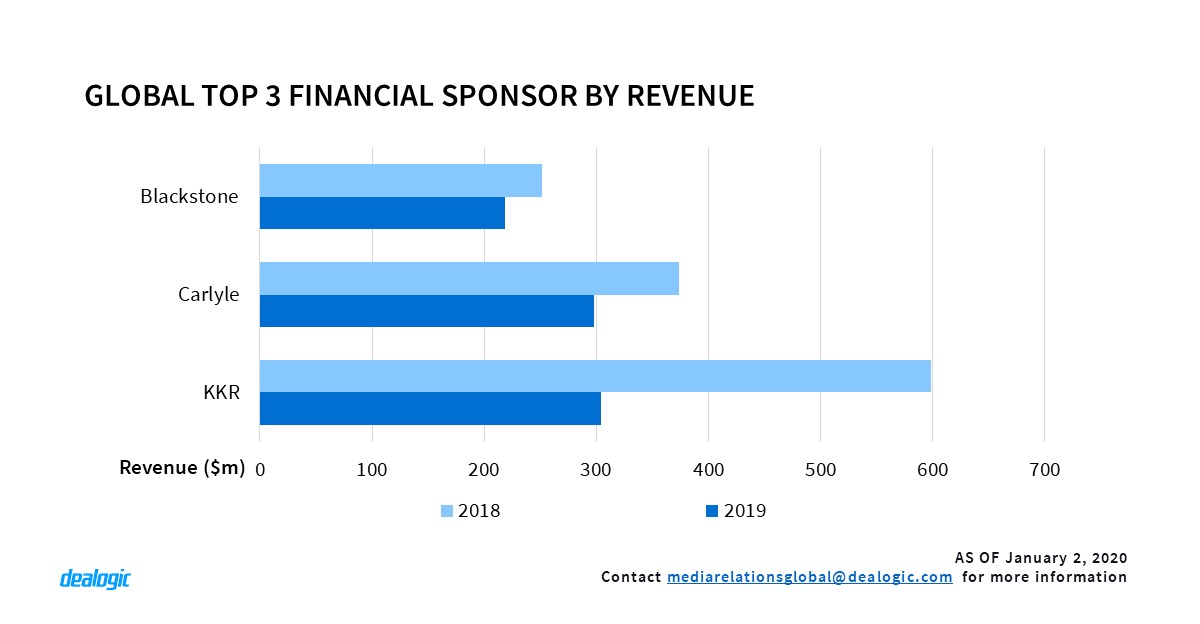

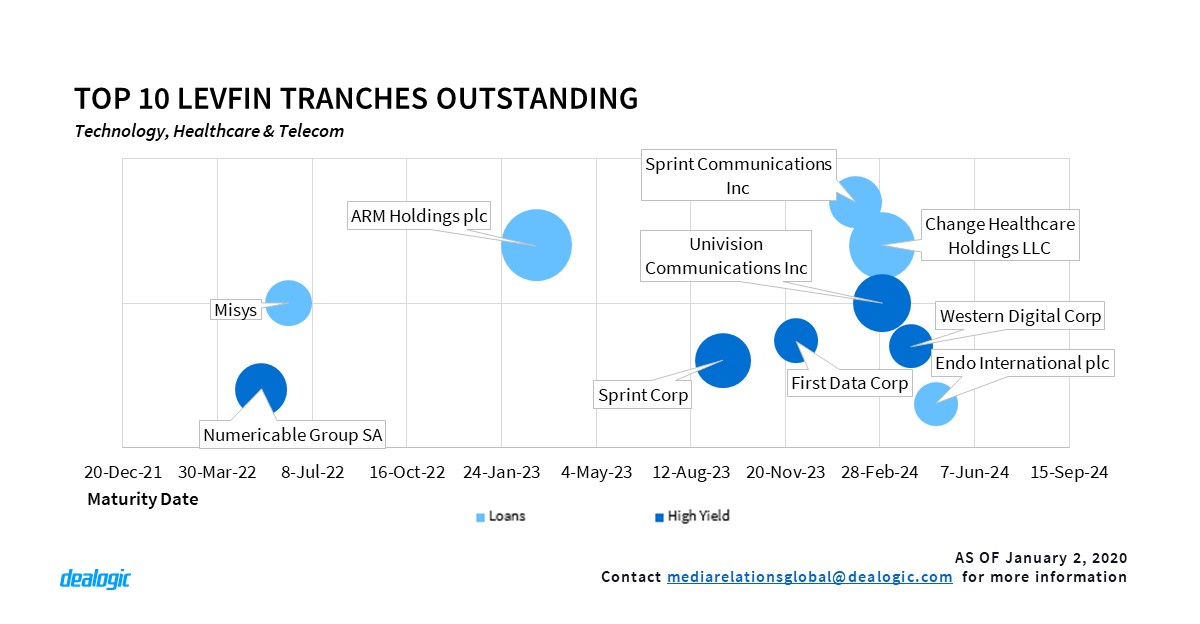

Technology kept its well-established first place in 2019, with $1.45bn of fees paid and a 16.4% share of overall wallet. This comes as no surprise as the technology sector has been a significant outperformer in the US equities market as well, up 41.8% compared to the S&P 500’s 25.3% rise [Footnote 1]. Clearly, investors remain attracted to the sector. Technology was followed by telecoms (13.3%) and healthcare (10.7%). Over the past 5 years, these 3 sectors contributed the most in terms of revenue paid. From a Financial Sponsor perspective, Carlyle Group climbed from 2018’s 2nd place to become the top fee payer in 2019 with a 3.5% share, generating $313m via 28 deals. Apollo Global Management and Platinum Equity followed, with a 2.7% and 1.9% share respectively. With $451.4bn coming due from these top 3 sectors, and a debt wall totaling $88.1bn for the top 3 sponsors in the next 5 years, this will fuel future opportunities.

US IG: Falling Margin Takes 2019 to a Runner-Up Spot

The major theme in the US markets has been the decline in interest rates over the past year, as US 10-year paper started the year yielding 2.56% and now yields 1.80%. The 3-month libor rate followed the same pattern and decreased from 2.79% to 1.91%. The reasons for the drop-in rates can be traced back to a slowdown in the global economy due to trade wars and political uncertainty.

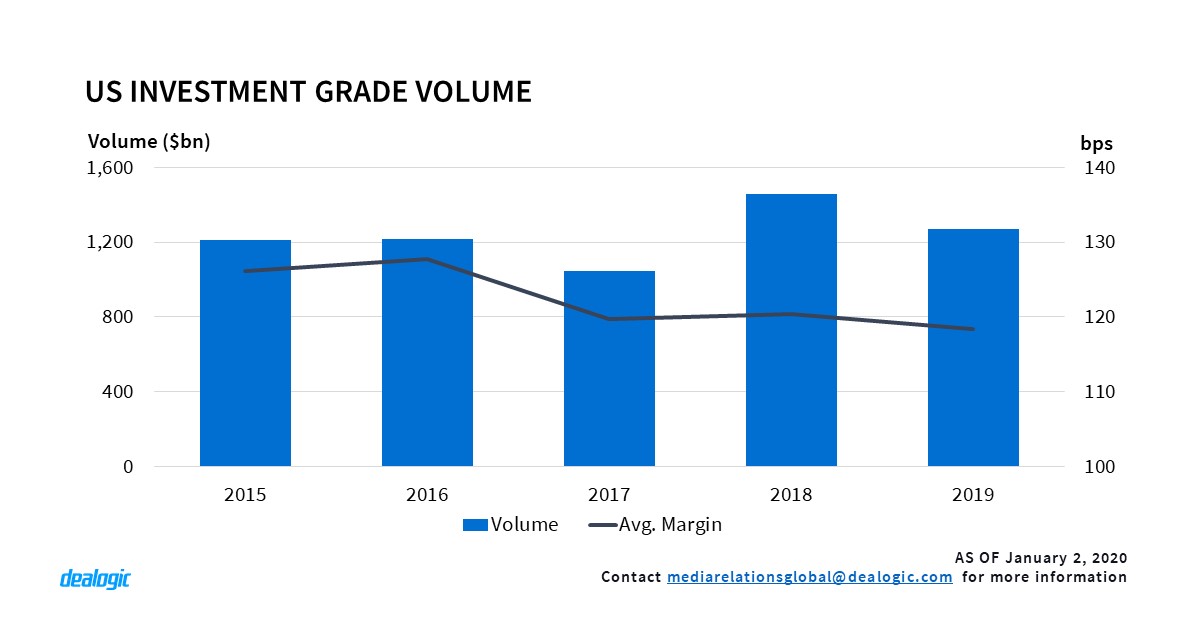

The US investment grade (IG) loan market was not spared from this uncertainty as volumes fell 13% year-on-year. US IG loan margins followed US interest rates and libor, falling slightly from 120bps in 2018 to 118bps in 2019. Low margins helped cushion any fall in volume, making 2019 ($1.27tr via 933 deals) the second highest for volume in the last five years.

While US IG borrowers again made refinancing the number one use of proceeds, US IG refinancing volumes were still down 12% year-on year despite lower libor rates and lower average margins across the US IG loan space. Another use of proceeds that saw a considerable decrease from the previous year was acquisitions, down 24% year-on-year in volume and 45% year-on-year in deal frequency. Were it not for the healthcare and oil & gas sectors, this decrease would have been much worse, with healthcare US IG loan acquisition volume increasing 108% and oil & gas volume increasing 367%. The increase in oil & gas was solely driven by the $35.6bn Occidental Petroleum Corp deal to pay for their purchase of Anadarko Petroleum Corp. Both lenders and investors in the US will be watching any trade war developments to look for an improvement in sentiment in order to take advantage of the decreasing rates and US IG loan margins.

EMEA: Climate Change and Sustainability Brighten a Lackluster Year

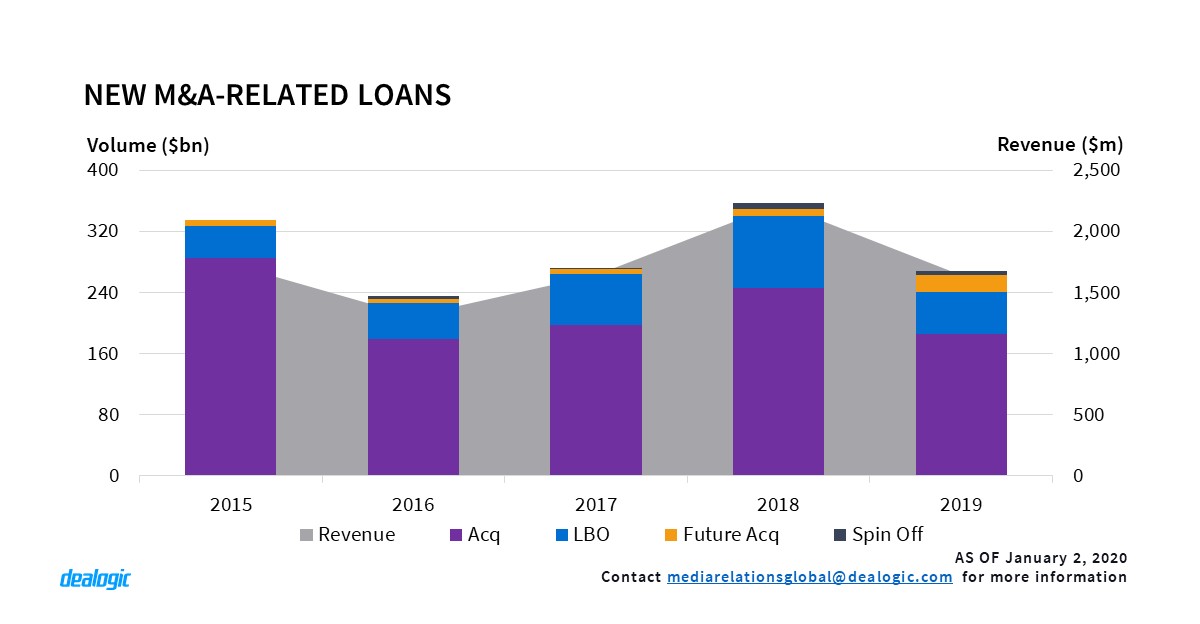

After two years of continuous growth, which saw volume jump by 15% and 31% in 2017 and 2018 respectively, Europe marketed new M&A-related loans contracted by 25%, leading to a reduction in revenue from $2.2bn to $1.6bn, year-on-year. A muted leveraged loan market, which saw LBO falling by 40% year-on-year, heavily dragged volume down. Jumbo [Footnote 2] M&A-related loan transactions, such as the London Stock Exchange Group’s $13.3bn acquisition of Refinitiv, Infineon’s $10.8bn acquisition of Cypress Semiconductor and the Tesareo $9.5bn acquisition by GlaxoSmithKline, cushioned the fall in volume. In fact, the 60 Jumbo M&A deals in 2019 accounted for 69.0% of the total volume. However, 2019 saw 24 fewer jumbo deals and a decline in their share of total volume by 8 points, as compared with 2018. The performance of M&A-related loans, reflected 2019’s lackluster year for the region which faced strong headwinds as a result of political uncertainties.

Despite, Brexit being the white elephant in the room, the EMEA market witnessed an exponential growth in ESG-linked and green facilities which jumped from $41.3bn in 2018 to $112.3bn in 2019. The driving sectors were Utility and Energy and Oil & Gas with $26.3bn and $12.3bn respectively. ESG-linked RCF was the impetus of this growth and accounted for 78.7% of the market.

North Asia and Southeast Asia Resist Falling APAC Volume

Loan volumes marketed in APAC were down 6% year-on-year, from $774.3bn to $730.2bn, and were the lowest since 2010. Except for Southeast Asia, loan volumes for all APAC regions decreased in 2019, in line with the decline in loan volumes globally and the region’s GDP growth slowdown from 5.5% in 2018 to 5% in 2019 [Footnote 3].

Australasia was the biggest contributor to the dip, with volume falling by 26%, well above the region’s average rate of decline. North Asia and South East Asia were the only regions which grew in 2019 with volume jumping from $247.2bn to 249.7bn and $85.5bn to $101.5bn, respectively. Across most Southeast Asian countries, loans volume increased. Jumbo facilities like Pengerang Petrochemical’s $9.3bn buyer’s credit helped significantly to increase volume. Issued to help finance the building of the largest downstream chemical plant in Asia, it accounted for 40.0% of Malaysian volume. For North Asia, Project Finance and capital expenditure, up by 18%, was a key driver for the region’s growth.

Refinancing, as usual, was dominant in the regions, despite 2019 volume falling to $268.0bn from 2018 ($265.3bn). The reduction in refinancing volume was, to some extent, due to fewer facilities available for refinancing. With $1.60tr of loans coming due in the next 5 years however, the market should see more refinancing opportunities. The trend for lower margins in some segments, like investment grade which fell from 122.21bps to 93.91bps year-on-year, will appeal to borrowers. With lower borrowing costs in APAC, the market should expect to see more borrowers taking advantage of this golden window, especially for companies with good credit quality. As already seen, Tencent’s $6.5bn refinancing loan allocated with a very tight margin of 80bps surpassed the initial ask of $5bn. Similarly, Alibaba successfully completed an amendment and extension of its $4bn loan signed in 2016, cutting the margin from 110bps to 85bps.

Finally, there is appetite for loans from lenders in the region as well. Foreign banks are even participating on local currency deals; like Taiwan’s Yunneng Wind Power Co Ltd $2.7bn loan which was 3 times oversubscribed. With liquidity available, a healthy debt wall and borrowers able to negotiate tighter margins, the region could see better volume ahead.

Footnote:

- Data source: Yardeni Research Inc

- Jumbo deals – loans that are equal or greater than $1.0bn

- Data source: IMF

– Written by Dealogic Loans Research

Data source: Dealogic, as of January 2, 2020

Contact us for the underlying data, or learn more about the powerful Dealogic platform.