Vodafone’s ratings game

Vodafone Group’s €18.4bn takeover of Liberty Global’s German and central European divisions has been labeled a daring move by some market participants. In response to Vodafone’s plans, Moody’s announced earlier this month a review for downgrade of the UK telecom conglomerate’s Baa1 rating. Considered equally bold, Vodafone’s financing scheme of the acquisition includes hybrid debt securities. This funding strategy aims at securing Vodafone’s investment-grade credit rating, according to the company’s official press release.

Until the first call date do us part

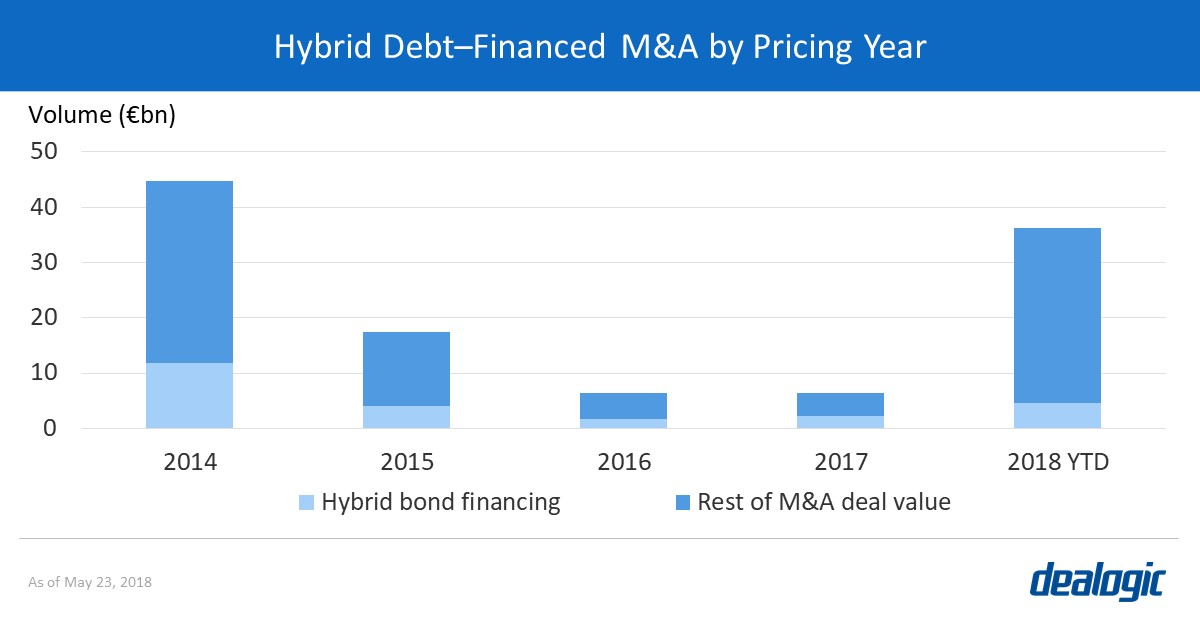

Hybrid security–backed acquisitions are not entirely foreign to corporates across the globe. Since 2014, more than €24bn in hybrid deals served as acquisition financing for €111.0bn worth of M&A deals. During this period, the biggest hybrid financings were done in 2014 by the healthcare sector’s Bayern AG, used for its purchase of Merck’s consumer-care business, and Orange SA (Vodafone’s French telecom competitor) for funding its acquisition of Spanish Jazztel. Each acquirer issued €3bn+ worth of hybrid debt.

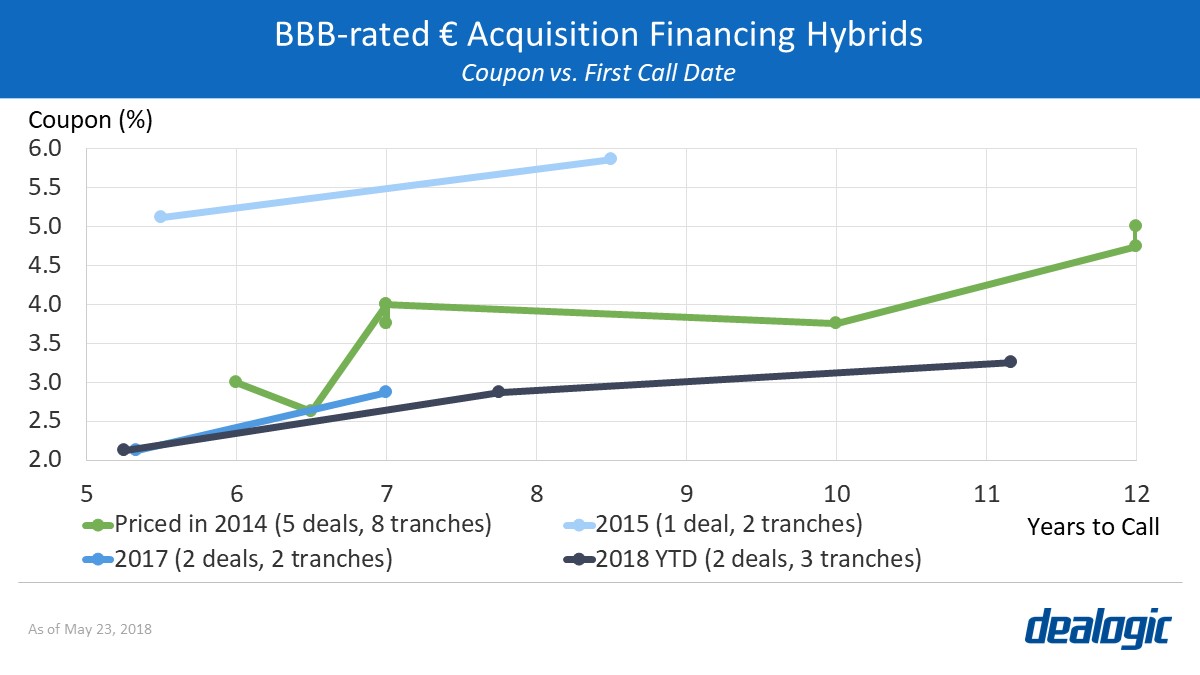

Hybrid financing helps to mitigate the credit impact of a future acquisition, as it receives equity credit status from rating agencies, hence helping the company’s leverage ratio. These perpetual and long-dated deals launched since 2014 feature call options with an average of 7.36 years. They allow issuers to seek more cost-effective financing options within a reasonable time.

Euro-denominated hybrid acquisition financing within Vodafone’s BBB league was silent in 2016, and lackluster in 2017. Taking into account the first call date of these hybrid trades, 2018 YTD offers such issuers lower coupons compared to the previous 4 years.

What’s next?

Vodafone is a familiar name on the bond market, with its longest-dated bond maturing in 2056. Until 2022, €17.2bn of debt is coming due from Vodafone and its subsidiaries in the form of bonds, loans, and convertibles. Based on the company’s press release, the acquisition of Liberty Global’s continental European operations will be funded by a package including €10.8bn in cash consideration, €3.0bn in mandatory convertibles, and €10.0bn in debt facilities—including hybrid securities.

Next in the pipeline with a similar funding scheme is Japanese Takeda Pharmaceutical, who also plans to use hybrid funding in relation to its €65.9bn acquisition of UK-based Shire. Markets are closely watching the execution of these two deals. If they are successful, other acquisitive corporates may follow their lead.

– Written by Anikó Nistor

Data source: Dealogic, as of May 23, 2018

Contact us for the underlying data, or learn more about the powerful Dealogic platform.