Global Perspective

Macroeconomic factors had a major impact on global IPO issuance in 2019 Q1. Global IPO volume stood at $17.3bn via 222 deals, representing a 65.8% decrease from 2018 Q1 ($50.5bn via 369 deals) and a 67.8% decrease from 2018 Q4 ($53.7bn via 372 deals) as varied macro factors combined to produce an overall depressed level of global IPOs.

In the US, due to the Government Shutdown, the first IPO of the year took place on the 30th day of January when generally in the past, IPOs used to be priced on the second week of January. Trade tensions between the US and China also negatively impacted the IPO market with Chinese company IPOs standing at $5.6bn via 46 IPOs, the lowest quarterly volume since 2015 Q3 ($1.9bn via 10 IPOs). In the EMEA region the shadow of Brexit brought uncertainty leading to UK IPO issuance reaching only $152m via 3 deals.

Red Hot A-Share Convertibles

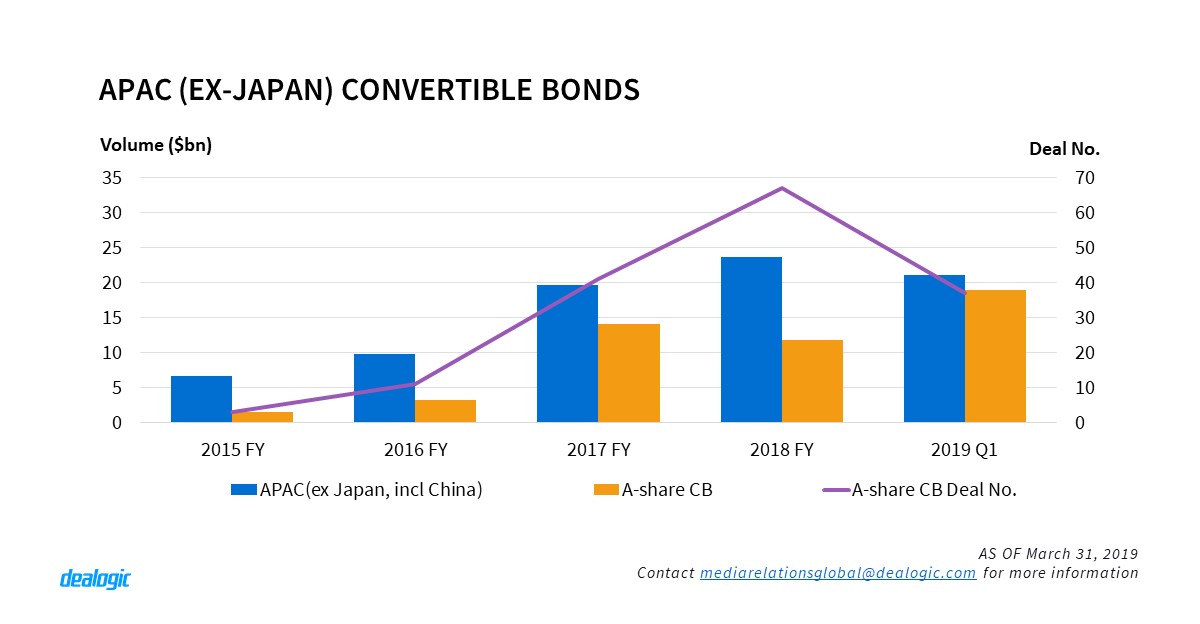

APAC (ex Japan) convertible bond annual volume reached $23.7bn last year, marking the highest level since 2010 ($27.0bn), and this momentum continued in the first quarter of this year. In 2019 Q1, $21.1bn was raised through 55 deals, setting a record-high Q1 convertible bond volume and highest Q1 convertible bond activity since 2006 (58 deals). One of the most notable deals this quarter was the Link REIT $510m green convertible bond, the first of its kind in the region and largest globally on record. But the main catalyst of the market is Chinese A-share convertible bond issuance that accounts for 90.0% of total APAC (excl. Japan) volume via 37 deals.

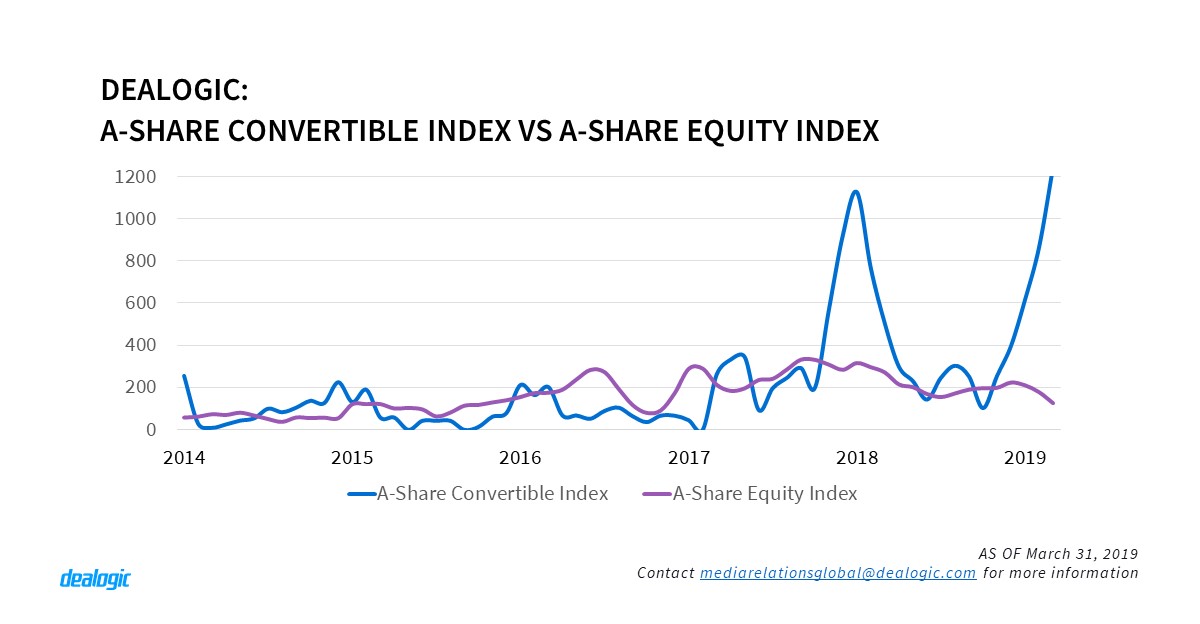

After the languishing performance in Chinese ECM market in 2018, the A-share convertible market has heated up and become the most popular equity-related capital raising instrument onshore as the Dealogic A-Share Convertible Index has risen to an all-time high of 1,246 in March while the Dealogic A-Share Equity Index, at 124, is at its lowest level since November 2016.

A-share convertible issuance makes up 39.8% and 75.5% of the onshore deal activity and volume respectively and has outpaced 2019 Q1 IPO volume by 6.4 times. In the first three months, A-share convertible bonds raised a record high of $18.9bn, resulting in a 59.4% and 34.0% increase compared with the full year volume in 2018 and 2017 respectively.

The promising A-share convertible performance is driven by issuance from 3 banks replenishing Tier 1 capital – China CITIC Bank Corp Ltd ($6.0bn), Ping An Bank Co Ltd ($3.8bn) and Bank of Jiangsu Co Ltd ($3.0bn) – contributing 67.7% of the total onshore convertible volume. Among the above deals, China CITIC Bank Corp Ltd issued the largest A-share convertible bond on record. More banks are planning to join the rally and with Shanghai Pudong Development Bank Co Ltd (approx. $7.9bn) and Bank of Communications Co Ltd (approx. $9.5bn) also lining up in the pipeline, the largest A-share convertible bond is still yet to be determined. (Footnote 1 & 2)

New Listings Braking

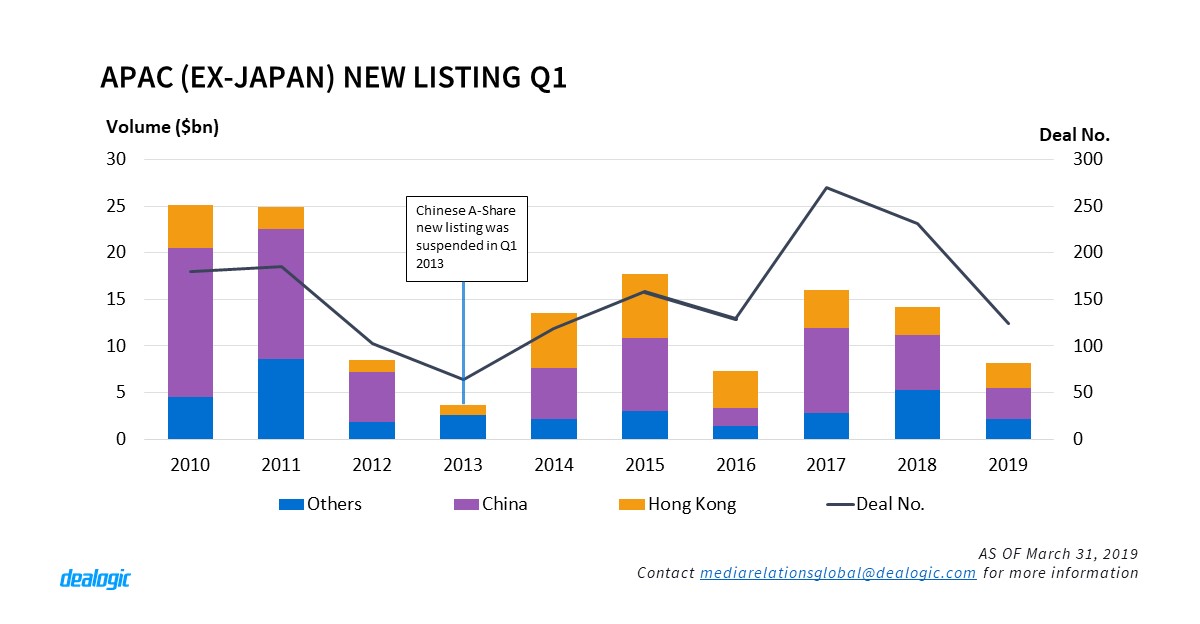

The new listings in APAC (ex Japan) saw its worst Q1 performance since 2016 under uncertain market conditions, with $8.2bn raised via 124 deals. The region recorded 42.3% and 44.6% decrease in both volume and activity comparing to 2018 Q1. The reason of the slowdown is mainly caused by the significant drop in Hong Kong and China A-share listings.

After a record-breaking listing performance in 2018 FY ($36.7bn via 202 deals), Hong Kong has suffered from a slow start in 2019 Q1 ($2.7bn raised via 34 deals) – the lowest Q1 volume since 2003 ($1.1bn via 10 deals). The volume of listings in Hong Kong is expected to decrease as there is no sign of mega/billion-dollar listings (e.g. $7.5bn China Tower listing and $5.4bn Xiaomi Corp listing in 2018) announced so far.

New listings in China is in deep water with $3.3bn raised via 27 deals in 2019 Q1, 43.5% and 20.6% drop in volume and activity compared to 2018 Q1. China Securities Regulatory Commission (CSRC) has applied a stricter listing approval process to enhance listing quality since early 2018, leading to a gradual decrease in listing activity for 4 consecutive quarters from 2018 Q1. The listing activity did recover a bit in 2019 Q1 from 2018 Q4, but the launch rate of new listing has come down to an average of 2 deals per week in 2019 Q1 (compared to 8 deals and 3 deals in 2017 Q1 and 2018 Q1 respectively). Although new listings in China are slumping, the activity is likely to pick up after the introduction of the Shanghai Sci-Tech Innovation Board in February. 28 companies (Footnote 3) have already submitted its IPO application to the Shanghai Stock Exchange for examination.

Political instability shakes EMEA ECM and pulls down IPO market to a 10-year low

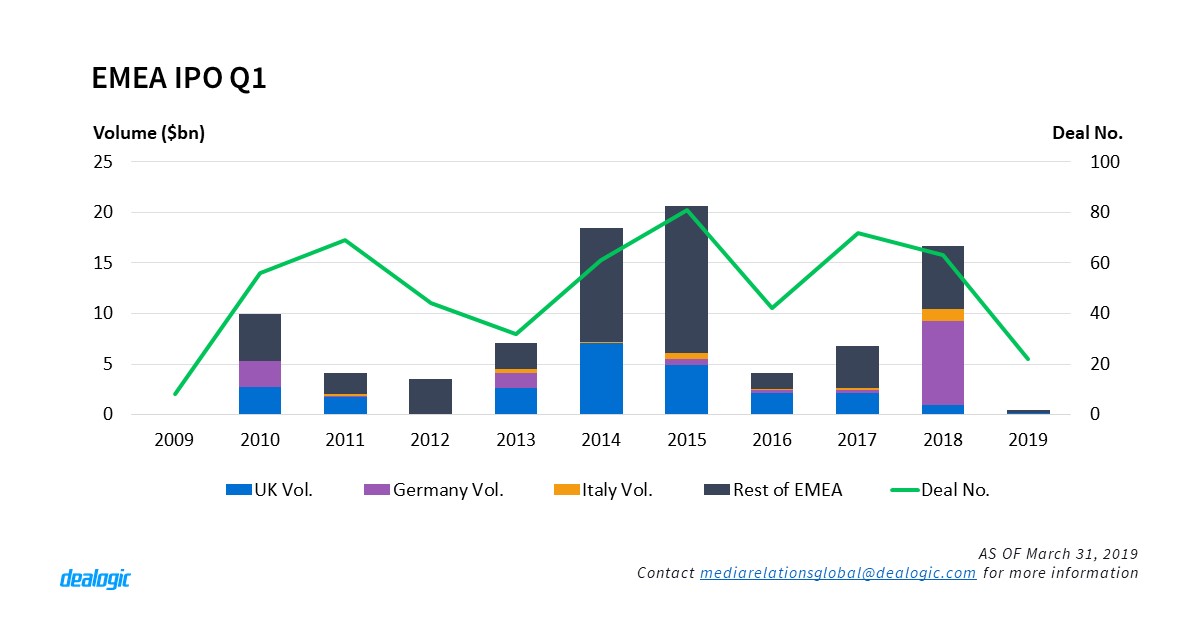

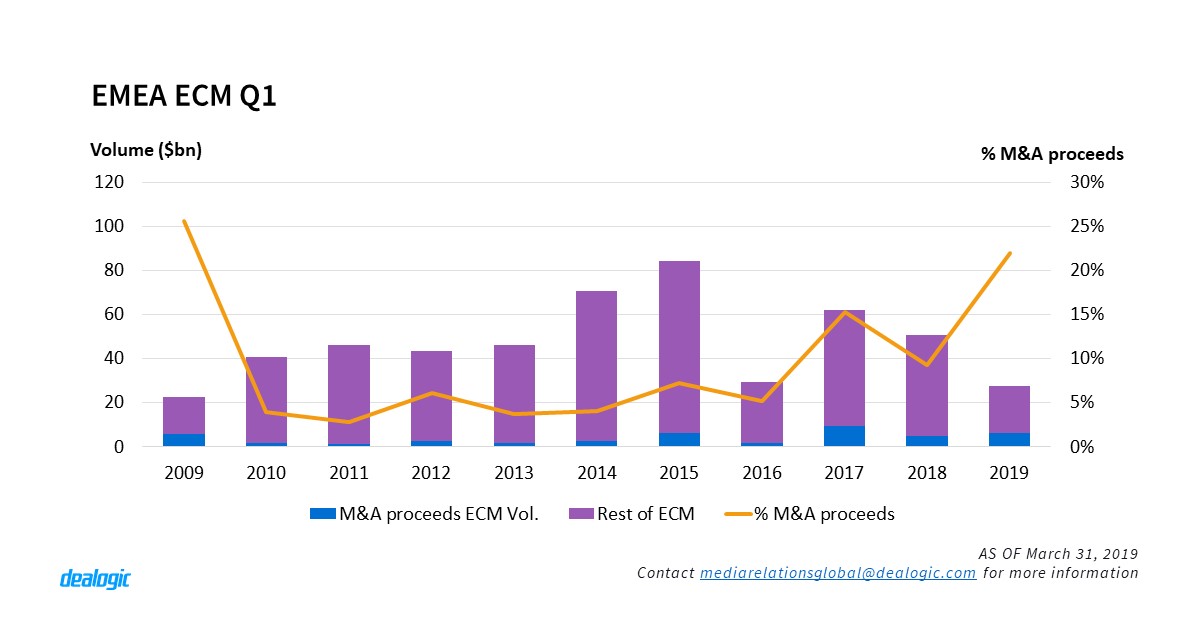

2018 was without doubt a tough year for EMEA ECM with a range of macroeconomic uncertainties affecting both investors’ and corporates’ sentiment. Their ongoing presence was reflected in the first quarter of 2019 that saw the lowest EMEA ECM volume ($27.7bn) for a Q1 since 2009 Q1 ($22.4bn) and the lowest activity (273 transactions – Footnote 4) since 2016 Q1 (234 transactions), while EMEA IPO levels dropped 97% to $475m in proceeds and 65% to 22 IPOs in activity compared to the same period last year with IPO proceeds this quarter standing as well at a 10-year low since 2009 Q1, when EMEA issuers generated only $83m via 8 flotations.

In contrast to 2018 Q1, when the EMEA IPO market was boosted by $1.0bn plus listings, in the first three months of 2019, the largest EMEA IPO-DWF Group plc-generated a total of $124m. Brexit’s deadlock and the rising political uncertainty in the region along with global trade tensions held back EMEA issuers from new flotations and investors from European equities. Earlier in March and citing the current market conditions, German automaker Volkswagen announced the postponement of its truck unit IPO, Traton SE, while payment firms’ Network International Holdings and Nexi Spa upcoming listings in London and Milan respectively, have brought back some optimism.

With a strong pipeline ahead, EMEA markets look forward to a big float to up volume and whet investors’ appetite. Although the UK led 2019 Q1 ECM IPO volume rankings, it saw its lowest IPO proceeds and activity in a Q1 ($152m via 3 IPOs) since 2012 Q1 ($71m via 3 IPOs), with the majority of UK flotations expected to be launched in the second half of the year, when it is hoped to have more clarity. Germany, which led the IPO proceeds in 2018 Q1 ($8.3bn via 7 IPOs) was absent from the top 10 ranking tables for the first time in a Q1 since 2014 Q1. Italy, which is ranked in fourth place in 2019 Q1 EMEA IPO proceeds after Saudi Arabia ($57.6m) and Malta ($55.2m), leads activity with 6 IPOs raising a total of $55.1m.

EMEA Acquisition-related ECM on rise

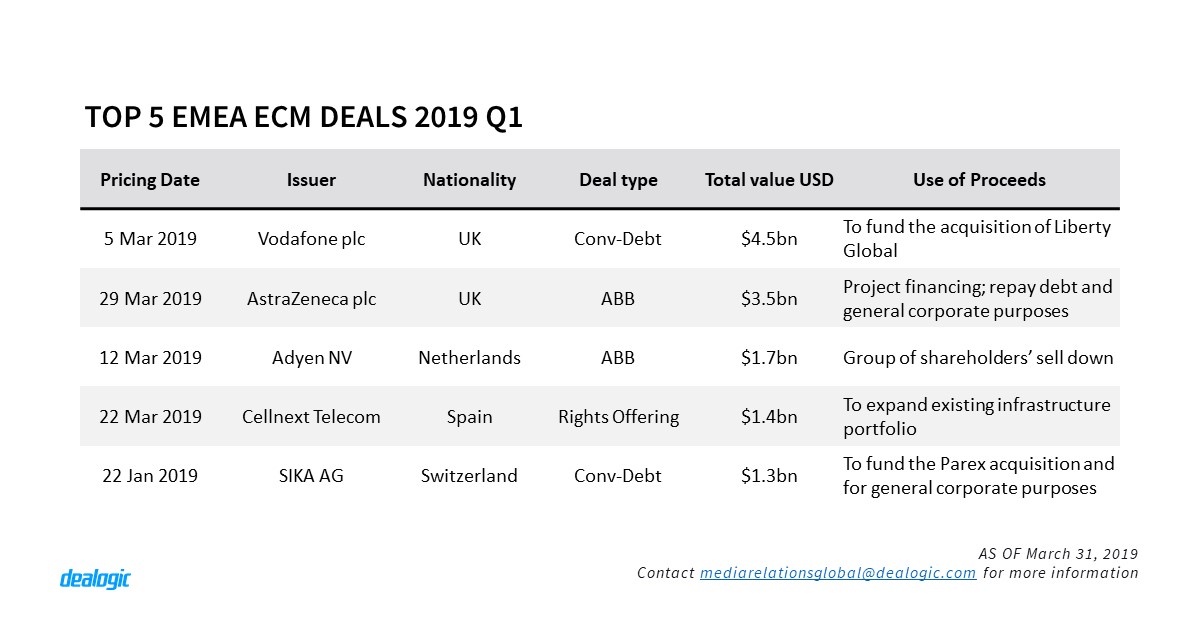

On March 5, UK telecommunications company Vodafone plc priced the largest EMEA ECM deal of 2019 Q1, Vodafone Mandatory Convertible Bond (Footnote 5), raising a total of $4.5bn (£3.4bn) to fund its acquisition of Liberty Global’s assets in central and Eastern Europe. The two-tranche deal is the largest EMEA convertible since Kwf’s exchangeable into Deutsche Telekom’s shares ($5.1bn) in 2008 and the largest ever sterling convertible bond. By combining the deal with derivatives from the banks that allow it to buy back shares at a hedged price, the company has sold a total of $2.4bn to investors with the rest allocated to the banks.

The deal along with SIKA’s convertible ($1.3bn) and Takeaway.com (FO/CONV) simultaneous offering ($775m), issued to fund the Parex and Delivery Hero acquisitions respectively, have boosted the acquisition-related ECM volume in 2019 Q1to $6.1bn via 25 deals, which accounted for 22% of the total EMEA ECM proceeds and 9% of its total activity, a 10 year-high for a Q1 in volume since 2009 Q1 (26%)and up 13 percentage points from 2018 Q1’s level .

The telecommunications sector occupied the first position on the EMEA ECM acquisition-related volume rankings for 2019 Q1 ($2.6bn via 3 deals), followed by the chemical sector on the second ($1.8bn via 2 deals) and the technology sector on the third place with $1.0bn via 8 deals, leading thus in activity.

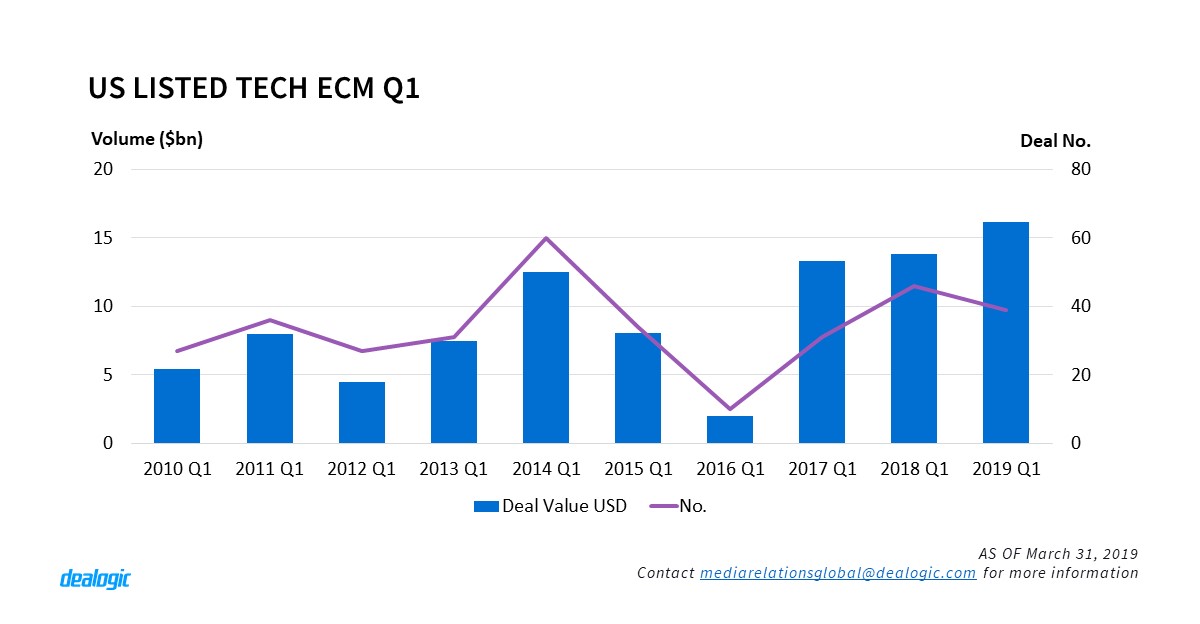

US Listed Technology Continues to Push for New High

In 2019 Q1, ECM volume from the US Technology sector reached $16.2bn via 39 deals, marking the second highest Q1 volume on record after 2000 Q1($48.3bn via 160 deals) during the high of the dot-com bubble. Cross-border issuance accounted for 35% of this total. Out of the top 5 Tech deals, three were cross-border issuances.

The biggest deal of the quarter for the Americas region was also executed by a tech company. On March 28th, Lyft Inc raised $2.3bn via NASD. This represents the biggest Tech IPO since the PagSeguro Digital Ltd IPO on January 23rd, 2018 for $2.6bn. Lyft Inc initially set a price range of $62-$68, due to high demand, they revised it up to $70-$72 and priced it at $72.

With Chinese regulators setting up the Science and Technology Innovation Board in Shanghai to entice Chinese tech companies to stay onshore rather than conducting IPOs offshore on US or HK exchanges, we could see a potential impact on future cross-border issuances. Currently, there are 15 Tech IPOs in the pipeline: 4 out of the 15 are from China from well-known companies like Yunji.Inc. US tech firm Pinterest Inc also officially filed their IPO on March 22nd. The success of Lyft Inc’s IPO has sparked its rival Uber Inc to go public soon as well.

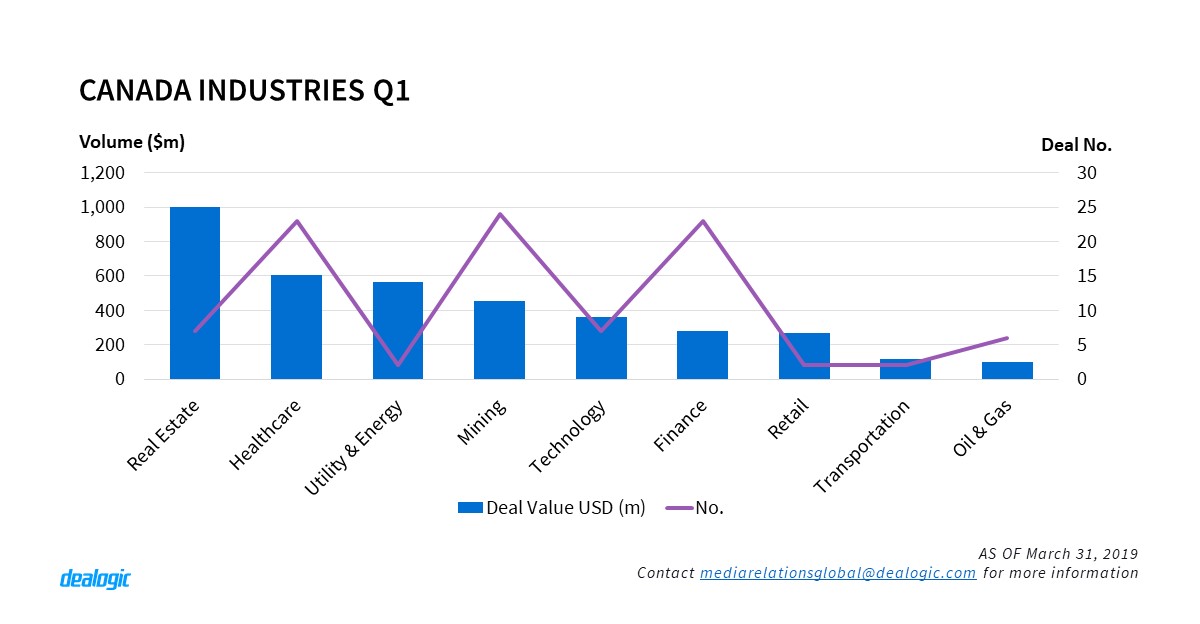

Canada Real Estate overtakes Cannabis ECM in Q1

Canada ECM saw a steady but rather peripheral growth in 2019 Q1. The Cannabis industry, whose volume has already reached $607m that is 40% of its $1.5bn deal value in 2018, still drives the Canadian market and is considered to be a significant player in the field. However, it was dethroned by the Real Estate industry that has experienced an incredible 203% upsurge by raising $998m in 2019 Q1 compared to last years’ $491m revenue.

Despite the ongoing neck and neck race between the Cannabis industry and Real Estate the largest deal in the region so far was Northland Power Inc’s secondary Bought Deal offering, raising $563m.

- Index Base Period: 2011 Average Monthly Issuance = 100

- DL A-Share Equity Index consists of IPOs & FOs

- Data Source Sci-Tech Innovation Board. As of March 29, 2019

- Vodafone transaction is referred as one deal in this report.

- On volume charts credit only the eligible tranches. For Vodafone convertible only the $2.4bn sold in the market is eligible

– Written by Dealogic ECM Research

Data source: Dealogic, as of March 31, 2019