Bond markets slow down

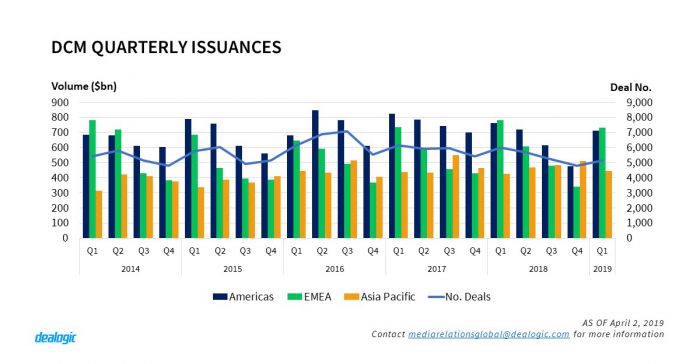

Global DCM markets started 2019 with moderate performance, as the first quarter of the year saw a 4.4% decrease with respect to the same period in 2018. A total of $1.89tr was sold in Q1 via 5,152 deals (vs. $1.97tr and 6,012 in Q1 2018). Despite a year-on-year decline, the current issuance represents an improvement with regards to the last quarter of 2018: a hefty 42.1% increase compared to $1.33tr distributed in Q4 2018. The bond volume issued in Q1 fares better than deal activity, which was the lowest in the past nine years. Compounding both variables, the resulting data shows the highest average deal size of the decade: $365.9m.

Looking at regional performance, it is EMEA markets where investors bought more paper, a total of $729.6bn from 1,552 deals. The region had a strong January, with $320.8bn of issuance. In Americas a total of $710.2bn was sold via 2,006 transactions and in Asia Pacific $445.4bn worth of 1,594 bonds was sold to investors. APAC region was the only one showing year-on-year growth, a 4.3% increase compared to Q1 2018. Americas and EMEA DCM volume went down 6.7% and 6.8%, respectively.

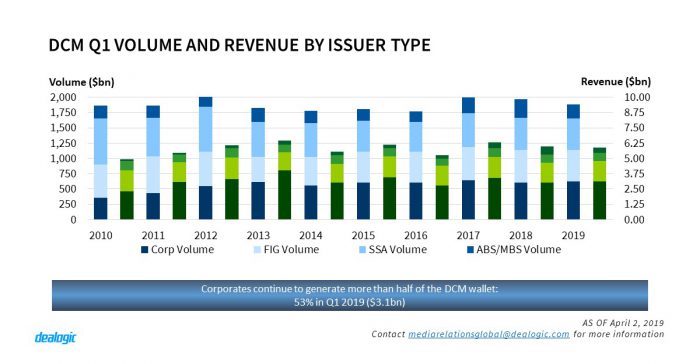

The reasons for the curb in the market can be found when data from different issuer types is extracted. Corporate issuers sold $623.4bn in Q1, keeping pace with the previous year (2.8% increase). FIG borrowers placed $513.1bn, 3.8% less than Q1 2018, and SSA issuance went down 0.5% to $517.1bn. Nonetheless, it is the securitisation market were performance went down significantly, from $312.3bn sold in 2018 to $226.1bn in the first quarter of this year (a 27.6% dip). All types of collateral were affected: especially CDO/CLO issuance went down 38.7% to $45.6bn and residential mortgages volume declined 27.8% to $80.9bn repackaged in Q1 of this year.

US dollar remains king

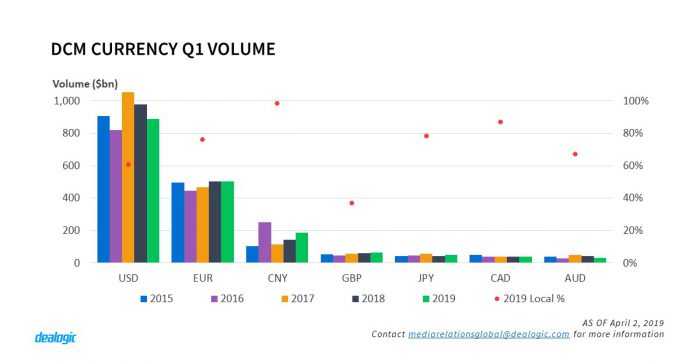

Issuance in US dollar totalled $886.4bn in the first quarter of the year, of which 60.9% was sold by local issuers. Tranches denominated in Euros reached $503.9bn, with a 76.4% domestic portion. From all the currencies at the top of the table the British pound is the currency showing the largest appetite from foreign borrowers: of the $62.9bn distributed amongst investors only 36.8% was sold by UK issuers.

The UK currency also provided another interesting feat in Q1: for the first time GBP-denominated volume using SONIA benchmark for FRN tranches surpassed the volume of those using Libor. Of the total $19.2bn of FRN issuance in British pounds $15.7bn will make coupon payments using SONIA.

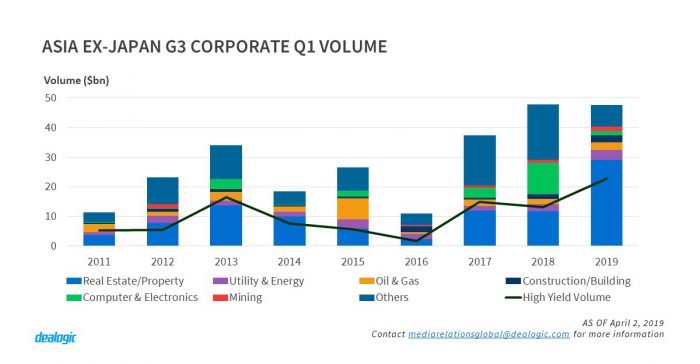

Asian G3 comes back

In Asia, the G3 market (ex-Japan) eventually saw a confident recovery from the downward trend since Q2 2018. Issuance on the first quarter of the year was $85.3bn, slightly higher than $84.8bn issued in the same period of 2018 and 13.3% lower than the record volume of Q1 2017 ($98.4bn).

While bond sales by the corporate sector didn’t move from the level of the previous year ($47.7bn issued in Q1 2019, 1% down year-on-year), high-yield issuance grew 73% to reach a record volume of $22.7bn. This was largely driven by the steady pricing activity of Chinese property developers, which has more than tripled the year-on-year volume to $19.3bn.

Another notable trend in the region was the placement of sustainable finance bonds, with a record Q1 volume of $12.1bn. While China has always led the way, Southeast Asia saw a surge driven by the second visit of the Indonesian government to the market. A $750.0m green tranche was launched at the same time of the year as the $1.25bn green debut of 2018. In addition, Australia is on track to form the Australian Sustainable Finance Initiative that aims to reshape the financial system to deal with climate change, in one of the strongest signs sent by the industry to prove that is taking the threat of global warming seriously. The group will be overseen by the Australian Prudential Regulation Authority (APRA).

EMEA tops DCM in Q1, but it tones down from previous years

In EMEA, Sovereign borrowers followed the annual credit cycle and came back strongly to the market in Q1: a total of $329.2bn of SSA paper was sold to investors, 3.5% more than in the first quarter of 2018. Governments of Italy, Spain, France, Belgium and Qatar issued a total of $52.4bn worth of bonds, with almost half of it ($20.5bn) being sold by Italy.

Other asset classes in the region didn’t perform as well as SSA. The securitisation market shrank notably: from $38.7bn sold in Q1 2018 to $13.1bn this year. CLO sales continue to power the market, and $8.6bn were distributed in Q1 2019. This figure, nonetheless, falls short by 34.6% from the issuance achieved last year.

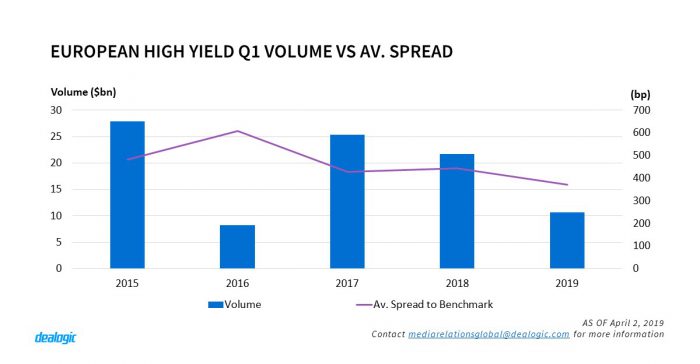

The corporate sector had a lacklustre first quarter too. Despite of some heavyweights in the Investment Grade area coming back to the market (Anheuser-Busch InBev’s $15.5bn, Orange SA’s €4.0bn, Daimler’s €3.3bn, Siemens’ €3.0bn) the overall corporate issuance of $150.5bn was 11.9% lower than the volume issued in the same period of the previous year. The fall is sharper when looking at Non-Investment Grade: only $16.3bn of junk debt was sold in the market in the first quarter of 2019, considerably lower than the volume distributed in 2018 ($32.8bn). The LevFin portion of the market space achieved $10.7bn worth of bonds sold this year.

US corporates show strength

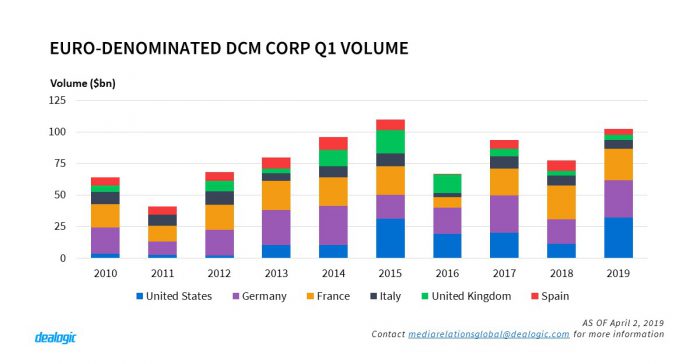

In the US, bond pricing has kept the same downward trend as in other markets. Whereas DCM issuance from US borrowers went down 4.0% year-on-year to $596.9bn via 1,766 deals, the US-marketed space -which includes cross-border issuers, had a more significant drop: a total of 1,834 deals worth $788.7bn was placed amongst US investors, 10.0% lower than the $876.3bn distributed in Q1 2018. Opposite to EMEA region, it is the corporate issuance sector that kept good pace this year. US corporates sold $241.9bn of debt in the markets, 21.6% more than the same period in 2018. They also made a strong return to the reverse yankee market: Medtronic priced €7.0bn of notes, IBM got €5.0bn allocated to investors and Altria €4.6bn. Overall, US corporates sold $32.3bn of euro-denominated debt, outperforming themselves in all previous first quarters, as well as German ($29.6bn), French ($24.7bn) and all other local corporations selling bonds denominated in euros so far this year.

Back in the US, the securitization market suffered a severe correction in 2019: issuance of US-marketed ABS/MBS went down 26.0% to $173.5bn sold to investors. The deterioration of the market comes from a sharp fall of CLO activity (41.8% down to $34.8bn distributed) and RMBS issuance (31.2% down to $54.7bn).

Outside the US, Canadian issuers had a better start to the year than in 2018, as $85.8bn of debt was sold in the first quarter of 2019 ($78.0bn in 2018). Latin American DCM, on the other hand, had the worst performance of the region: a 54.3% decline with only $27.6bn of bonds priced in 2019.

– Written by Dealogic DCM Research

Data source: Dealogic, as of April 2, 2019