Chinese banks join the perpetual club

On January 25th Bank of China sold a CNY40bn ($5.94bn) perpetual bond (perp) to investors in the onshore market. The deal is the first of its kind issued by a mainland commercial bank. It was well subscribed, as offshore investors were also able to purchase notes through Bond Connect, a platform that allows foreigners to buy onshore transactions by placing their orders via the Hong Kong stock exchange. With a bid-to-cover ratio of more than 2 the deal got distributed to over 140 accounts.

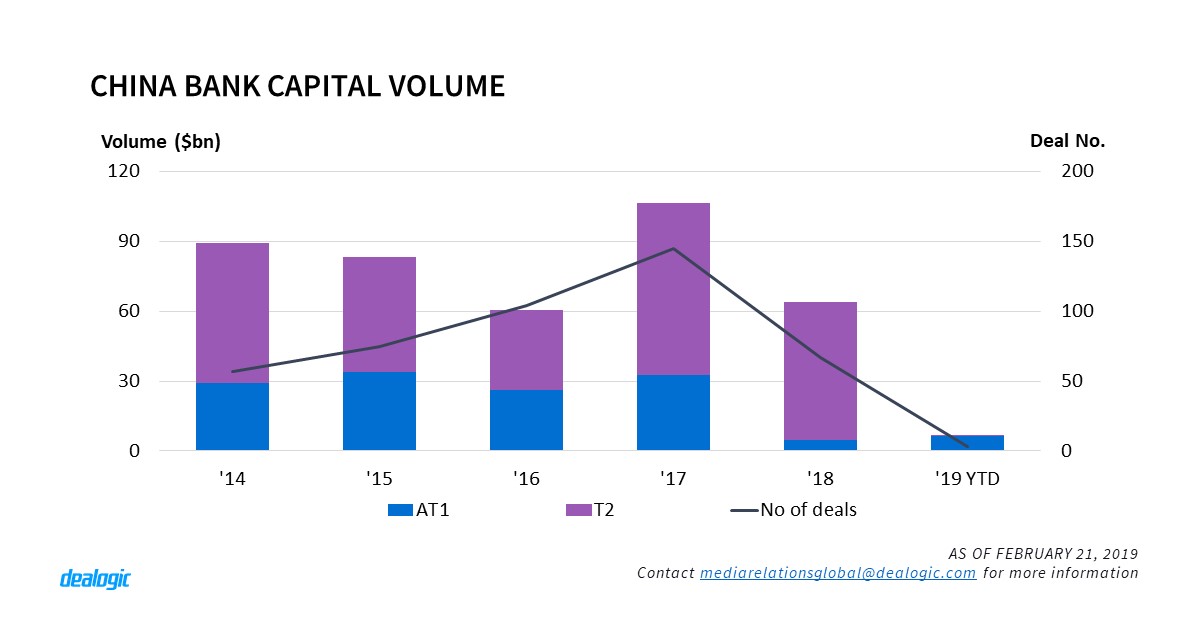

Commercial banks have issued perpetual bonds to supplement their bank capital since late 2014. Historically, mainland banks were not allowed to issue such an instrument, having to rely instead on private placements, equity IPOs and preferred stocks issuance to boost their capital. With Basel III, China banks’ additional tier 1 (AT1) capital volume has consisted of onshore and offshore preferred shares since 2014, being all of them perpetual deals. AT1 volume reached $32.8bn in 2017 (30% of the sum of AT1 + T2 capital), whereas only $4.9bn of AT1 issuance was sold in 2018.

Small players helped by more alternatives

According to the China Banking and Insurance Regulatory Commission (CBIRC), commercial banks are obliged to meet their capital ratio requirements by the end of 2018. They will need to maintain a minimum capital adequacy ratio (CAR) of 9.5% and a core tier 1 CAR of 8.5%. To help address its capital-raising needs, People’s Bank of China (PBoC) gave permission to Bank of China (BOC) to sell its perp debut in December and set up a central bank bills swap (CBS) programme in January. Meanwhile, that same month, CBIRC issued a short statement allowing insurance companies to purchase banks’ perps for the first time.

The big four commercial Chinese banks (Bank of China, Industrial and Commercial Bank of China, China Construction Bank and Agricultural Bank of China) have no immediate needs for raising bank capital, as their ratios are well above minimum requirement. For instance, BOC’s T1 capital adequacy ratio has reached 12.3% after its perp issuance. The new policies however, are good news to small and medium-sized banks, especially those with lower capital adequacy ratios. These expanded funding channels bring new methods to maintain capital ratios and solve any liquidity concerns.

China bank capital weighs heavily worldwide

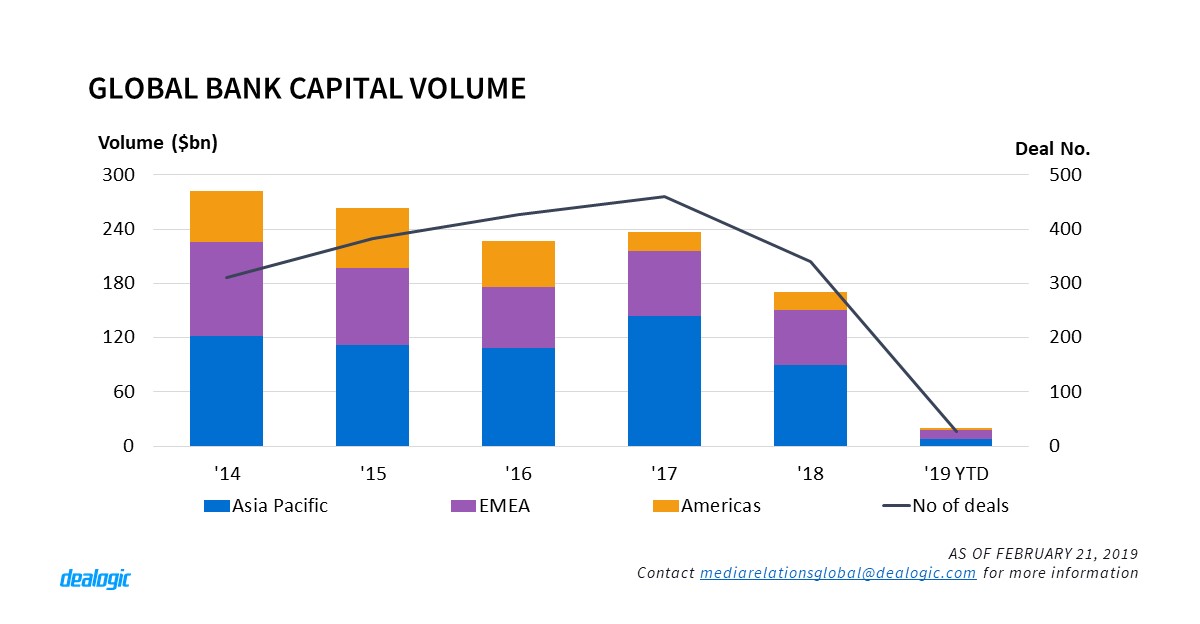

Chinese financial institutions have been major bank capital issuers and with these new policies their market dominance could increase. In 2018, the country saw $ 64bn worth of bank capital issued, which accounted for 69% of all APAC volume, distantly followed by Japanese and Australian banks ($8.9bn and $7.9bn respectively). Globally, China accounted for almost 37% of the total $173.6bn of bank capital volume marketed last year, leaving the United States behind, in second place, with a far lower $13.9bn. This year to date, with the help of the BOC’s perp jumbo deal, China volume has already reached $6.5bn, a notable 30% share of the global issuance.

– Written by Joshua Chen

Data source: Dealogic, as of February 20, 2019

Contact us for the underlying data, or learn more about the powerful Dealogic platform.