EMEA leaves it late and APAC remains quiet; valuations low

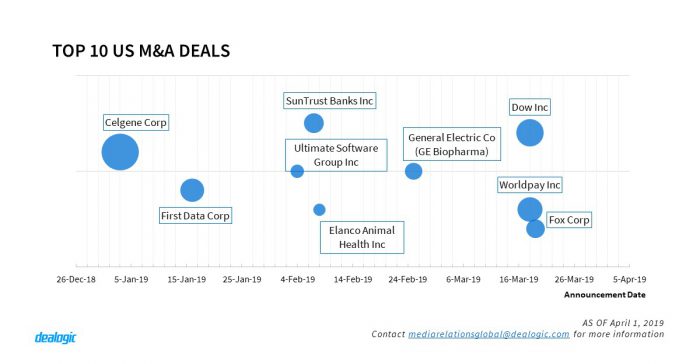

Q1 2019 started off in style, with Bristol-Myers Squibb announcing a $96.8bn offer for US-based Celgene Corp just three days into the new year. Since then global M&A volume has been somewhat underwhelming. However, a late volume resurgence during the last two weeks of the quarter has seen total global M&A volume accelerate, thanks to mega deals such as Saudi Aramco’s $69bn offer for 70% of SABIC, DowDuPont’s $52bn spin-off of Dow Inc and Fidelity’s $43.3bn acquisition of Worldpay, breathing life into a slow start to the year.

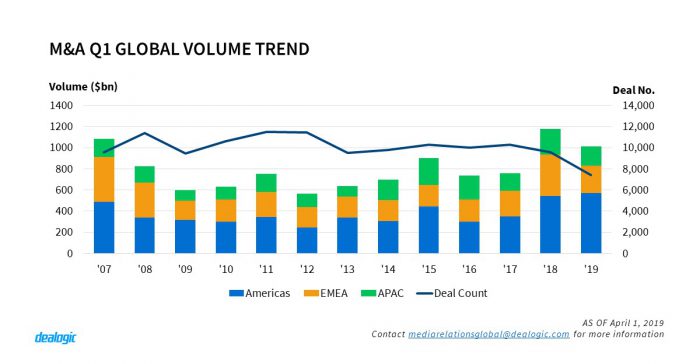

During Q1, global M&A volume reached $1.01tn via 7,470 deals, representing a decrease of 13.8% and 22.1% in volume and deal count, respectively, in comparison to the same period of 2018. Most notably, APAC targeted M&A has seen a decline in volume with just $179.5bn in volume recorded during Q1 2019, the lowest since 2017. EMEA however rebounded during the final days of Q1 due to the Saudi Aramco acquisition of SABIC, boosting EMEA volume to $261.4bn via 2,329 deals.

M&A “mega deals” have been in short supply across both regions with only 1 deal in EMEA above $10bn during Q1 2019. In contrast, the Americas account for 11 mega deals announced this YTD with 10 deals involving United States based targets accounting for 60.8% of total Americas targeted volume. Coincidentally, M&A valuations have also seen a gradual decline with the median EV/EBITDA multiples globally falling to the lowest level since 2012, at 12.01x. This fall in valuation could be enough to re-ignite the M&A fires and tempt investors into a wave of M&A deal making over the coming months.

Sponsor exits on the rise

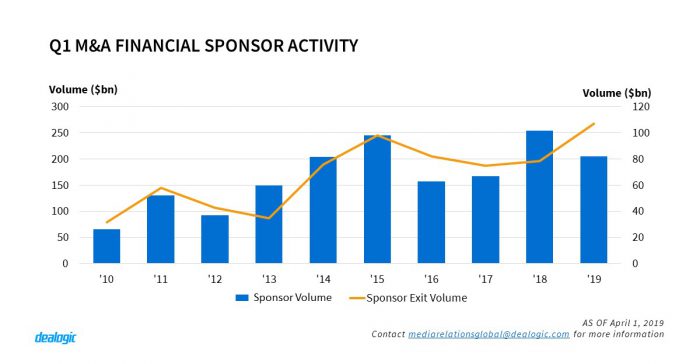

Despite the slow start of global M&A this year, the M&A Financial Sponsors market is keeping a steady pace with a global volume of $205.5bn; down by 18.2% from last year ($251.2bn) but still the third highest since 2010. The United States is in the lead with $114.0bn, representing 55.5% of all deal volume. Top volume driving deals this quarter include Fiserv’s acquisition of First Data Corp ($39.4bn), the acquisition of Ultimate Software Group Inc ($12.4bn) and CapitaLands’ offer for Ascendas and Singbridge ($8bn).

In Q1 2019, Sponsor M&A Exits reached a record high volume with $106.8bn, 37.6% higher than the previous year ($77.6bn) and still above the previous Q1 record in 2015 ($103.2bn). Looking at other sponsor exit alternatives – Equity Capital market IPOs and follow-ons – there was a decline since its peak in 2015 ($48.2bn from 119 deals) barely hitting $13.3bn in volume with 51 deals this year. The trend shows Financial Sponsors are more and more reliant on M&A transactions when planning their exits.

Slow Start of China M&A

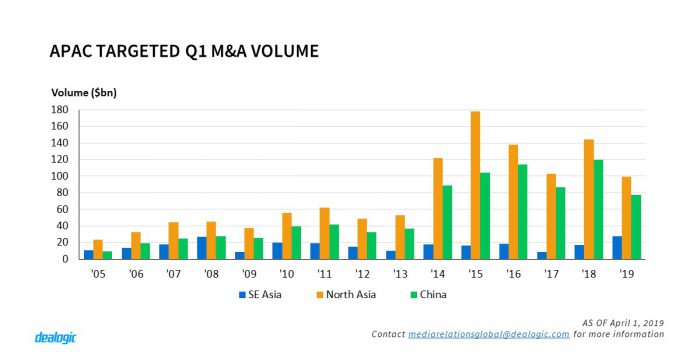

With rising protectionism in the region, the Asia Pacific-targeted M&A has had a slow start in Q1 2019 with M&A volume dropping to $180.2bn, down 25.9% from the same period in 2018. Within the region, the most active nation, China, has also seen a sharp slide in its China-targeted M&A volume to $77.8bn, representing a decrease of 34.8% in comparison to the same period in 2018 ($119.4bn). The valuation for China-targeted M&A has been declining for two consecutive years, with the median EV/EBITDA dropping to 17.8x in Q1 2019, the lowest since 2014 with 17.7x.

Return of Southeast Asia

Despite a global decline in M&A activity, Southeast Asia targeted M&A volume has started strong in 2019. With $27.4bn in volume via 245 deals, representing a 63.9% increase in volume compared to the same period in 2018 ($16.7bn via 284 deals), it reached the highest level on record. This is largely driven by CapitaLand’s $8.1bn acquisition of Ascendas and Singbridge in January and TMB Bank’s $4.2bn acquisition of Thanachart Bank in February, which ranked the largest and the fourth largest deals in Asia Pacific so far this year.

EMEA starts slowly; UK still ahead despite Brexit turmoil

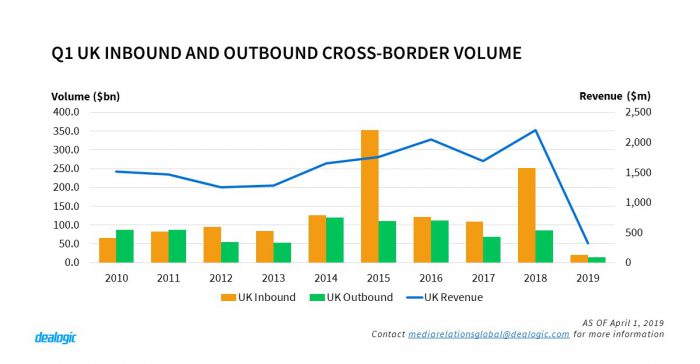

2019 M&A activity in EMEA started slowly, with $261.4bn in Q1 volume – a 33.5% decline from last year’s $393.2bn. Despite the slow start to the quarter, activity picked up in the end of March with the announcement of the acquisition of a 70% stake in Saudi Basic Industries Corp by Saudi Arabian Oil Co for $69.1bn.

The M&A market in Europe recorded its lowest Q1 volume since 2002 ($126.1bn), with $149.5bn in announced M&A volume generated so far this year. Nevertheless, two of the biggest countries continue as regional leaders, with Germany-targeted deals at $23.8bn, and the UK (aside above mentioned Saudi Basic Industries Corp mega deal) maintaining its lead position with $37.5bn in Q1 2019, despite the uncertainty around Brexit.

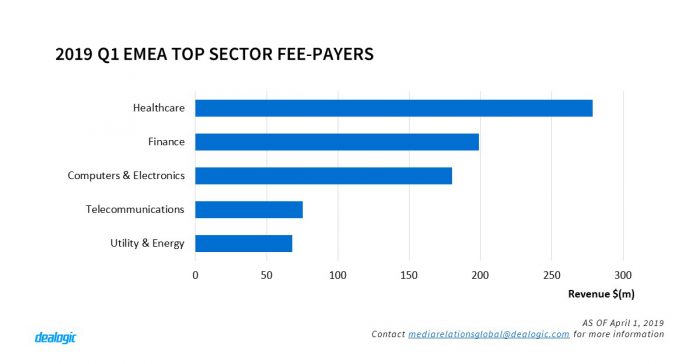

Chemicals took the lead as the most targeted sector in EMEA this quarter due to the announcement of the Saudi Basic Industries Corp transaction. The sector recorded $79.0bn in volume and $41.1m in revenue and is followed by technology with $34.3bn in volume and $180.1m in revenue. These are replacing last year’s top two: healthcare and telecommunications; which recorded only $6.5bn and $18.0bn in activity this first quarter, respectively.

US M&A

Within the Americas, US-targeted M&A shattered historical Q1 records by reaching a total volume of $537.6bn across 2,158 deals. With a plethora of mega-deals driving Q1 volume, US-targeted volume accounts for a staggering 93.7% of all Americas-targeted M&A volume during Q1 2019. Deals in healthcare, for the second consecutive Q1, have been the largest contributor to US M&A with $182.1bn in volume, and 33.9% of the market share. This is driven by Bristol-Myers Squibb Co’s offer to acquire Celgene Corp for $96.8bn, as well as Danaher Corp’s acquisition of GE Biopharma for $21.4bn. Technology, as usual, is the next most active sector, with its $131.7bn deal value representing a 24.5% market share in Q1 2019.

– Written by Dealogic M&A Research

Data source: Dealogic, as of April 1, 2019